Chapter 1 Static Models

1.1 Static Philips Curve

Lesson: Problematic analysis with a static model between inflation and unemployment

Set the Time Series

cd "/Users/Sam/Desktop/Econ 645/Data/Wooldridge"

use phillips.dta, clear

tsset year, yearly

reg inf unem if year < 1997/Users/Sam/Desktop/Econ 645/Data/Wooldridge

time variable: year, 1948 to 2003

delta: 1 year

Source | SS df MS Number of obs = 49

-------------+---------------------------------- F(1, 47) = 2.62

Model | 25.6369575 1 25.6369575 Prob > F = 0.1125

Residual | 460.61979 47 9.80042107 R-squared = 0.0527

-------------+---------------------------------- Adj R-squared = 0.0326

Total | 486.256748 48 10.1303489 Root MSE = 3.1306

------------------------------------------------------------------------------

inf | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

unem | .4676257 .2891262 1.62 0.112 -.1140213 1.049273

_cons | 1.42361 1.719015 0.83 0.412 -2.034602 4.881822

------------------------------------------------------------------------------Our result do not suggest a trade off between inflation and unemployment, and potentially suggest a positive relationship. This is likely a misspecified model and does not best describe the short-run trade-off between inflation and unemployment. We’ll look at an augmented Phillips curve that better describes the relationship.

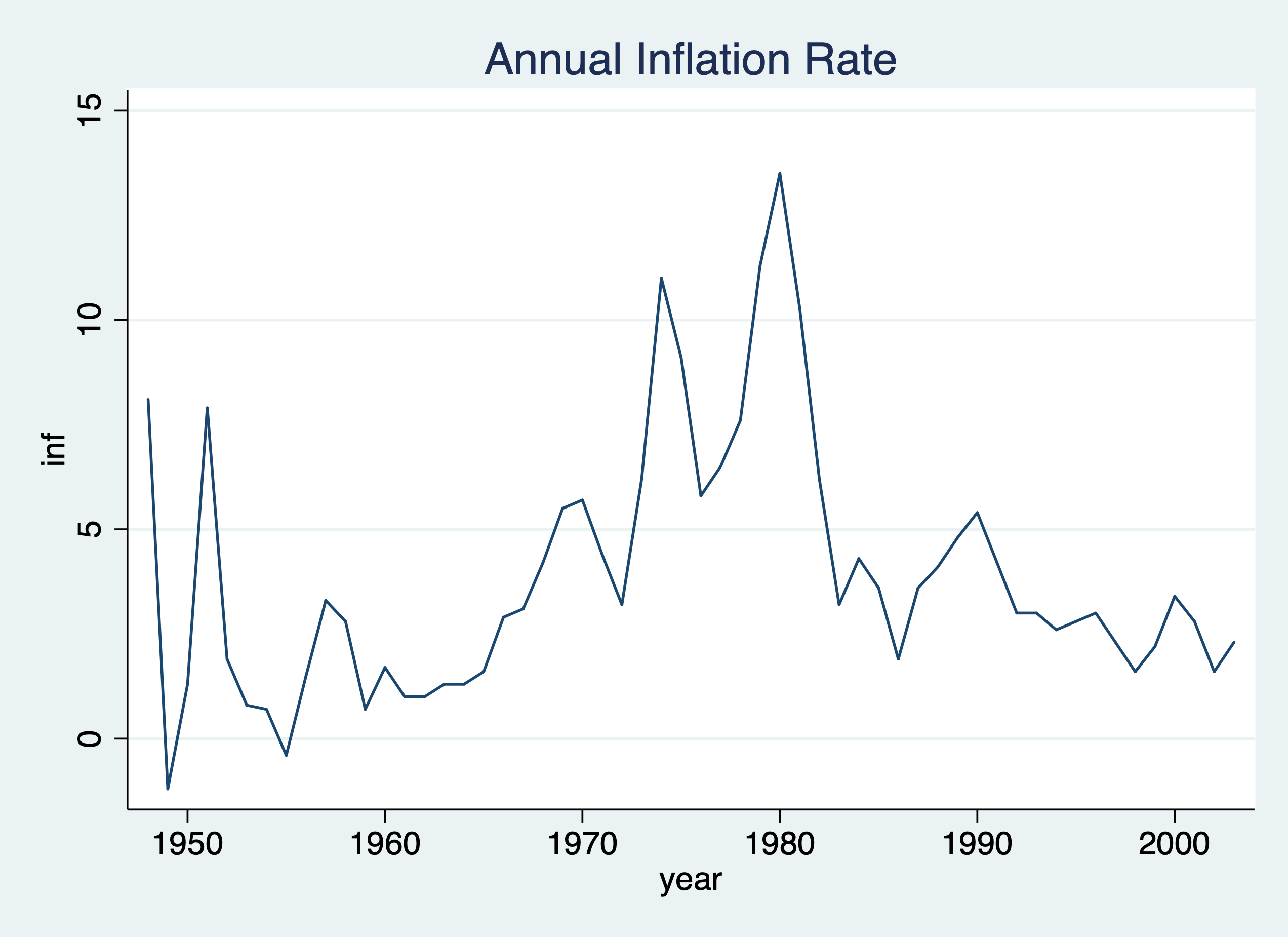

Let’s graph our time series

twoway line inf year, title("Annual Inflation Rate")

graph export "/Users/Sam/Desktop/Econ 645/Stata/week_10_inf_line.png", replace

We can use tsline as well.

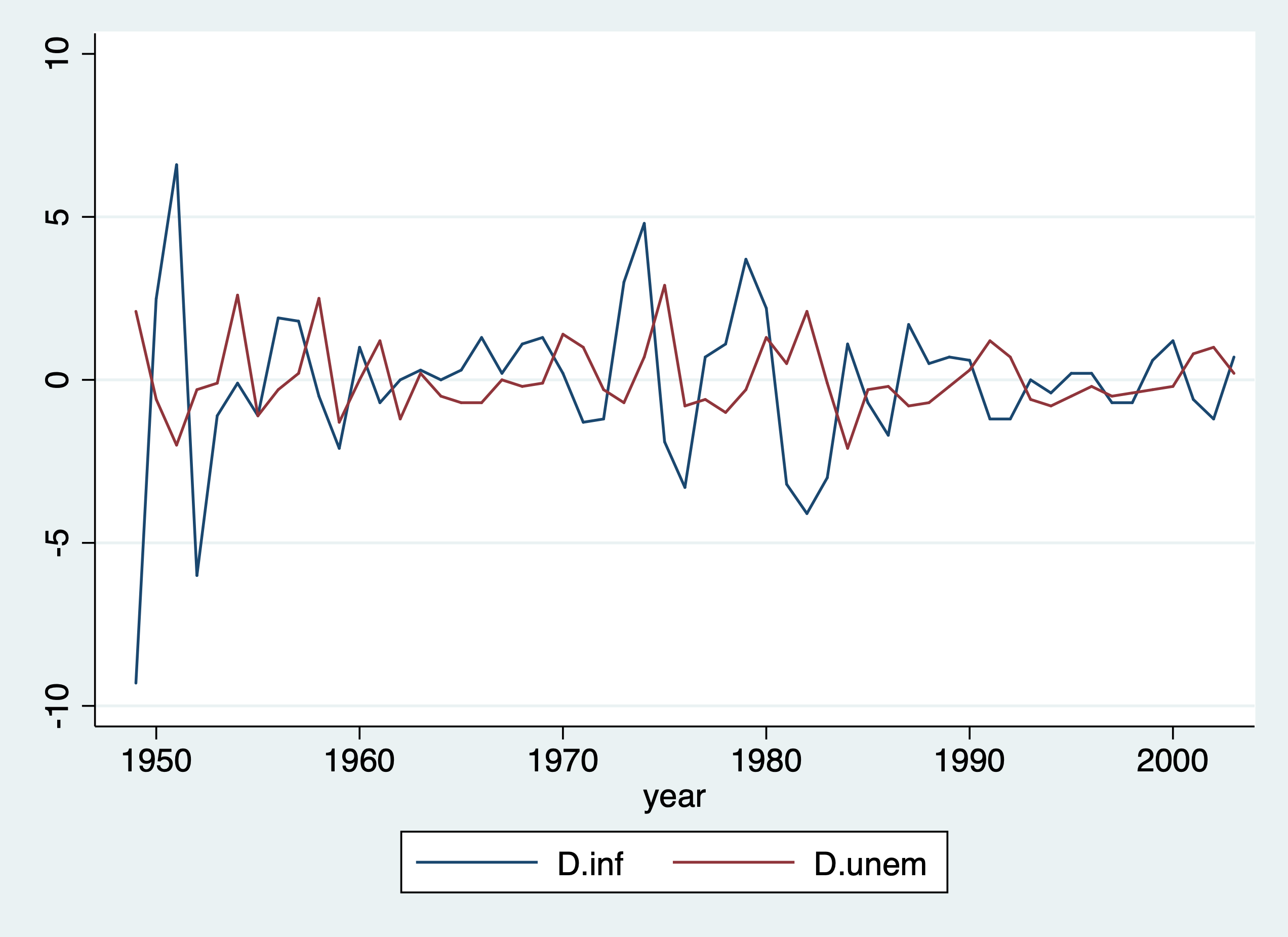

We can take the difference in the time series as well. Use the s. operator instead of d.. While s1 and d1 will produce similar results, s2 and d2 will not produce the same results.

tsline s.inf s.unem

graph export "/Users/Sam/Desktop/Econ 645/Stata/week_10_ts_Dinfemp.png", replace

Caution: \[ D2. \neq S2. \] It is not recommended to use d. beyond the first difference. Use the S12. operator If you are interested in \[ x_{t}-x_{t-12} = \Delta x \] D2 gives the difference in differences (not the research design. Such that the D2.operator calculates: \[ D2 = x_{t} - x_{t-1} - (x_{t-1}-x_{t-2}) \] \[ S2 = x_{t} - x_{t-2} \]

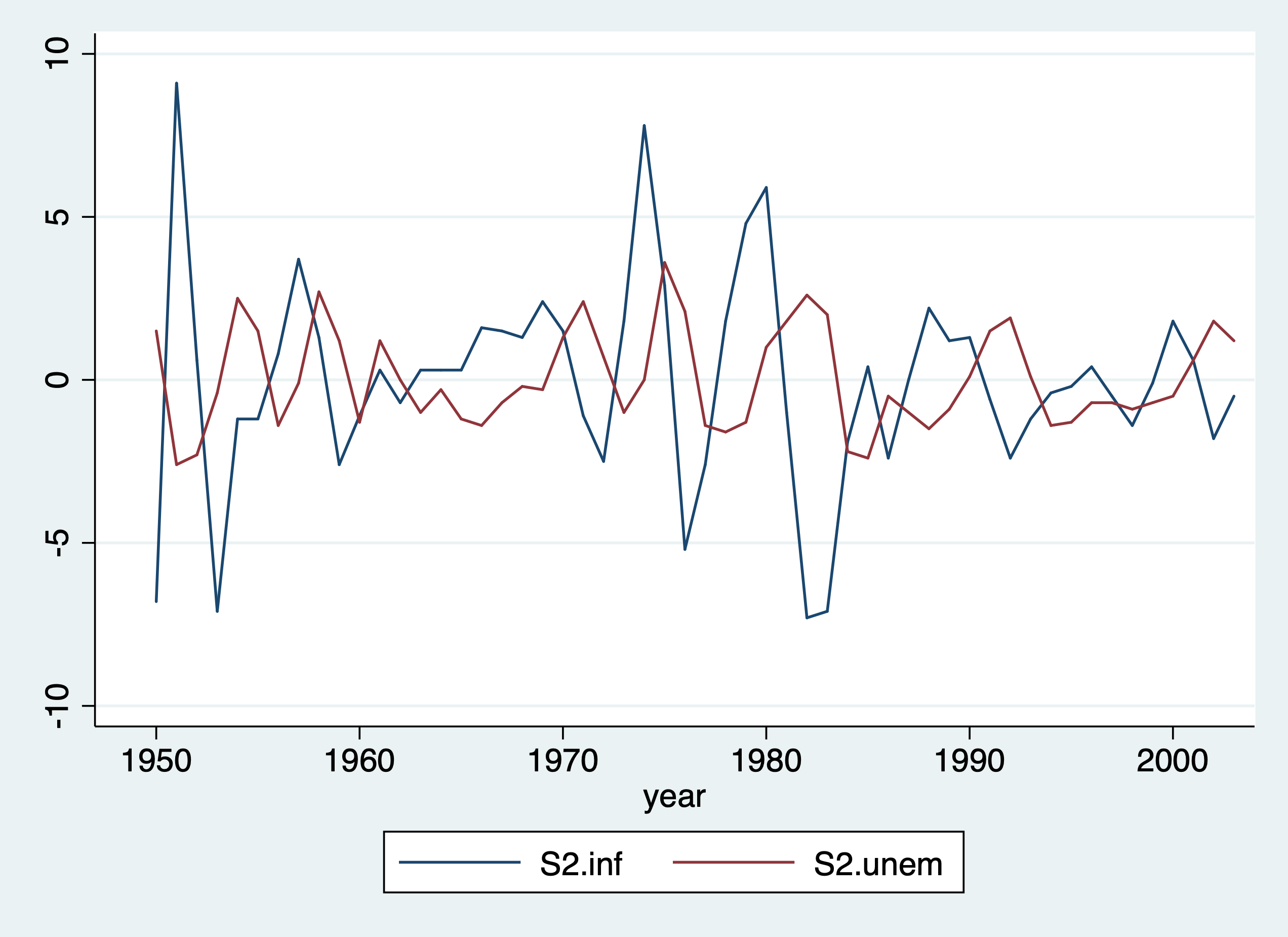

We can take the 12-month difference in the time series as well.

tsline s2.inf s2.unem

graph export "/Users/Sam/Desktop/Econ 645/Stata/week_10_ts_D12infemp.png", replace

1.2 Inflation and Deficits on Interest Rates

Lesson: some static models explain time-series better than the prior model

Looking inflation and deficits on interest rates, our model is: \[ i3_t = \beta_0 + \beta_1 inflation_t + \beta_2 deficitpct_t + u_t \] Where

- \(i3\): the 3-month T-bill rate

- inf: the annual inflation rate from CPI

- def: is the federal budget deficit as a percentage of GDP

Set the Time Series

cd "/Users/Sam/Desktop/Econ 645/Data/Wooldridge"

use intdef.dta, clear

tsset year

reg i3 inf def if year < 2004/Users/Sam/Desktop/Econ 645/Data/Wooldridge

time variable: year, 1948 to 2003

delta: 1 unit

Source | SS df MS Number of obs = 56

-------------+---------------------------------- F(2, 53) = 40.09

Model | 272.420338 2 136.210169 Prob > F = 0.0000

Residual | 180.054275 53 3.39725047 R-squared = 0.6021

-------------+---------------------------------- Adj R-squared = 0.5871

Total | 452.474612 55 8.22681113 Root MSE = 1.8432

------------------------------------------------------------------------------

i3 | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

inf | .6058659 .0821348 7.38 0.000 .4411243 .7706074

def | .5130579 .1183841 4.33 0.000 .2756095 .7505062

_cons | 1.733266 .431967 4.01 0.000 .8668497 2.599682

------------------------------------------------------------------------------This static model better explain interest rates based on basic macroeconomics. Both contemporaneous variables explain current interest rates. A 1 percentage point increase in the inflation rate leads to a 0.6 percentage point increase in the nominal interest rate. A 1 percentage point increase in the deficits as a percentage of GDP leads to a 0.5 percentage point increase in nominal interest rates.

1.3 Puerto Rican Employment and Minimum Wage

We’ll look at the association between employment and minimum wage in Puerto Rico. Our model will be: \[ lprepop_t = \beta_0 + \beta_1 lmincov_t + \beta_2 lusgnp + u_t \] Where

- ln(prepop): the natural log of the employment to population ratio in PR

- ln(mincov): natural log of the importance of minimum wage relative to average wages or mincov=average minimum wage/average wages)*average coverage rate or people actually covered by the minimum wage law

- lusgnp: natural log of US GNP

Set Time Series

cd "/Users/Sam/Desktop/Econ 645/Data/Wooldridge"

use prminwge, clear

tsset year

reg lprepop lmincov lusgnp if year < 1988/Users/Sam/Desktop/Econ 645/Data/Wooldridge

time variable: year, 1950 to 1987

delta: 1 unit

Source | SS df MS Number of obs = 38

-------------+---------------------------------- F(2, 35) = 34.04

Model | .211258366 2 .105629183 Prob > F = 0.0000

Residual | .108600151 35 .003102861 R-squared = 0.6605

-------------+---------------------------------- Adj R-squared = 0.6411

Total | .319858518 37 .008644825 Root MSE = .0557

------------------------------------------------------------------------------

lprepop | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

lmincov | -.1544442 .0649015 -2.38 0.023 -.2862011 -.0226872

lusgnp | -.0121888 .0885134 -0.14 0.891 -.1918806 .167503

_cons | -1.054423 .7654065 -1.38 0.177 -2.60828 .4994351

------------------------------------------------------------------------------Our results show that there is a tradeoff between the employment ratio and the importance of minimum wage. A one percent increase in importance of minimum wage the employment-population ratio declines .154 percent.

1.4 Antidumping Filings and Chemical Imports

The barium industry in the U.S. complained to the International Trade Commission that China was dumping (or selling imports at lower prices to undercut domestic producers). First, are imports unusually high before the complaint? Second, do imports change after the dumping complaint?

Our model is the \[ lchnimp_t = \beta_0 + \beta_1 lchempi_t + \beta_2 lgas_t + \beta_3 lrtwex_t +\beta_4 befile6_t + \beta_5 affile6_t + \beta_6 afdec6 + u_t \]

Where

- lchnimp: natural log of the volume of Chinese imports of barium chloride

- lchempi: natural log of domestic chemical production index

- lgas: natural log of gasoline production

- lrtwex: natural log of the exchange rate index

- befile6: binary for 6 months before a complaint filing

- affile6: binary for 6 months after a complaint filing

- afdec6: binary for 6 months after a positive decision

Set Time Series Monthly

cd "/Users/Sam/Desktop/Econ 645/Data/Wooldridge"

use barium.dta, clear

tsset t, monthly

reg lchnimp lchempi lgas lrtwex befile6 affile6 afdec6/Users/Sam/Desktop/Econ 645/Data/Wooldridge

time variable: t, 1960m2 to 1970m12

delta: 1 month

Source | SS df MS Number of obs = 131

-------------+---------------------------------- F(6, 124) = 9.06

Model | 19.4051607 6 3.23419346 Prob > F = 0.0000

Residual | 44.2470875 124 .356831351 R-squared = 0.3049

-------------+---------------------------------- Adj R-squared = 0.2712

Total | 63.6522483 130 .489632679 Root MSE = .59735

------------------------------------------------------------------------------

lchnimp | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

lchempi | 3.117193 .4792021 6.50 0.000 2.168718 4.065668

lgas | .1963504 .9066172 0.22 0.829 -1.598099 1.9908

lrtwex | .9830183 .4001537 2.46 0.015 .1910022 1.775034

befile6 | .0595739 .2609699 0.23 0.820 -.4569585 .5761064

affile6 | -.0324064 .2642973 -0.12 0.903 -.5555249 .490712

afdec6 | -.565245 .2858352 -1.98 0.050 -1.130993 .0005028

_cons | -17.803 21.04537 -0.85 0.399 -59.45769 23.85169

------------------------------------------------------------------------------We see that imports are not higher 6 months before a complaint, and imports are not lower 6 months after a complaint. However, imports are lower 6 months after a positive decision in a complaint by the ITC. The impact is fairly large and imports of barium chloride fall about 43.2% after a positive decision.

Also notice that rtwex is positive, and we would expect that a stronger dollar increase demand for imports, which is about uni-elastic.

-43.163985