Chapter 2 Forecasting

2.1 One-Step Ahead Model vs Dynamic AR(1) Model

One-step ahead we can use predict or forecast for AR(1). We use the estimates store command to store our results for our AR(1) model.

One-Step Ahead Model

We can get one-step ahead just using predict

Forecast - One-step-ahead forecast. We three addition commands:

- forecast create

- forecast estimates

- forecast solve

For a one-step ahead forecast, static is our key option otherwise it will not be a one-step ahead forecast.

Computing static forecasts for model forecast1.

-----------------------------------------------

Starting period: 1997

Ending period: 2003

Forecast prefix: st_

1997: .............

1998: .............

1999: ..............

2000: ..............

2001: ..............

2002: .............

2003: ............

Forecast 1 variable spanning 7 periods.

---------------------------------------

+------------------------------+

| year unem st_unem |

|------------------------------|

50. | 1997 4.9000001 5.5264521 |

51. | 1998 4.5 5.160275 |

52. | 1999 4.1999998 4.8673334 |

53. | 2000 4 4.6476274 |

54. | 2001 4.8000002 4.5011568 |

|------------------------------|

55. | 2002 5.8000002 5.0870399 |

56. | 2003 6 5.8193936 |

+------------------------------+Dynamic Model

Dynamic model - We won’t use l.unem but l.dy_unem

Computing dynamic forecasts for model forecast1.

------------------------------------------------

Starting period: 1997

Ending period: 2003

Forecast prefix: dy_

1997: .............

1998: .............

1999: ............

2000: ............

2001: ............

2002: ............

2003: ............

Forecast 1 variable spanning 7 periods.

---------------------------------------

+------------------------------------------+

| year unem st_unem dy_unem |

|------------------------------------------|

50. | 1997 4.9000001 5.5264521 5.5264521 |

51. | 1998 4.5 5.160275 5.6190596 |

52. | 1999 4.1999998 4.8673334 5.6868811 |

53. | 2000 4 4.6476274 5.7365503 |

54. | 2001 4.8000002 4.5011568 5.7729259 |

|------------------------------------------|

55. | 2002 5.8000002 5.0870399 5.7995653 |

56. | 2003 6 5.8193936 5.8190751 |

+------------------------------------------+Graph Model

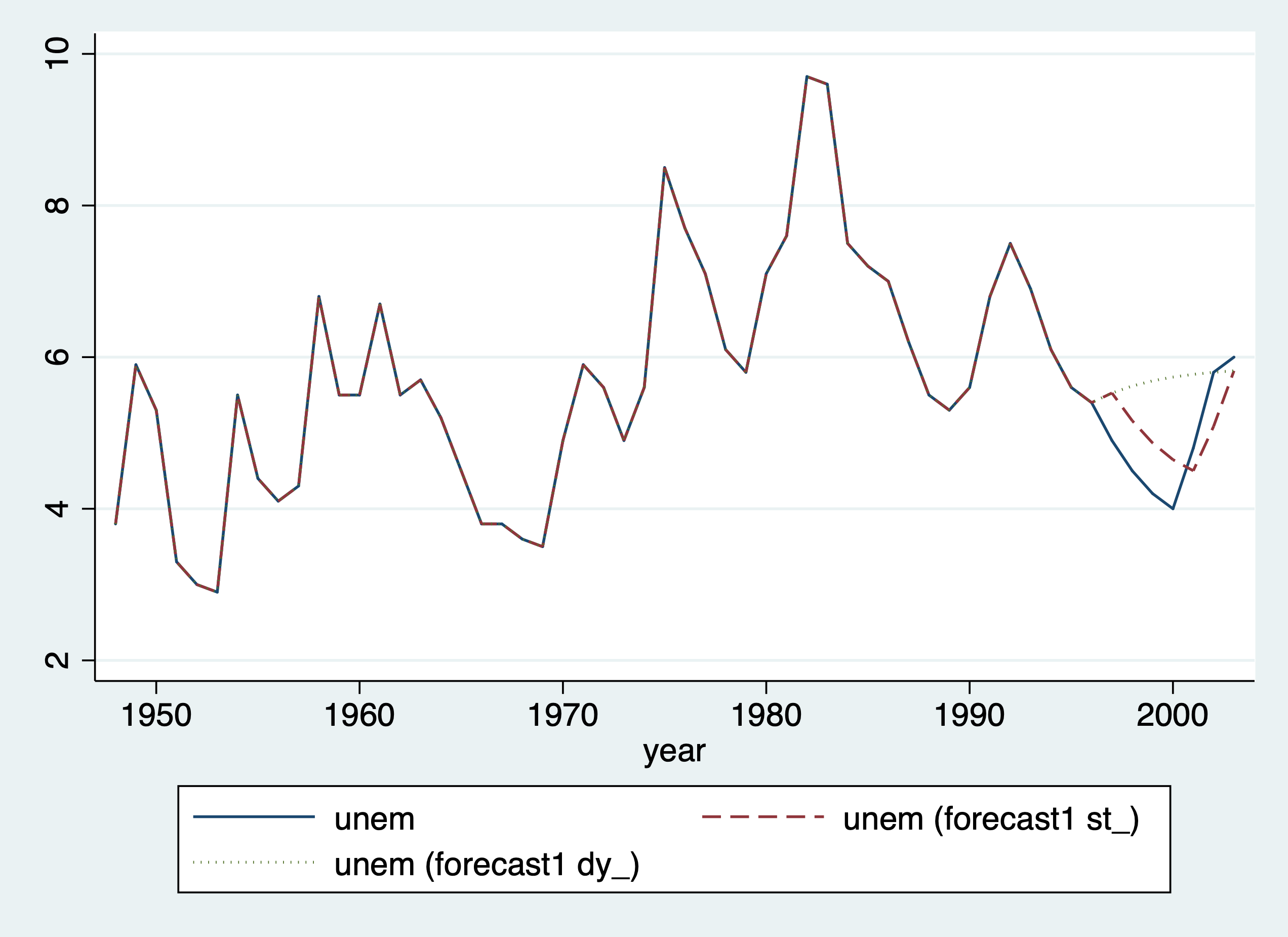

Graph Actual, One-Step-Ahead Model, and Dynamic Model

twoway line unem year || line st_unem year, lpattern(dash) || line dy_unem year, lpattern(dot)

graph export "/Users/Sam/Desktop/Econ 645/Stata/week_11_static_v_dynamic.png", replace

Root Mean Squared Error (RMSE)

Calculate RMSE for AR(1) model

gen e = unem - st_unem

gen e2 = e^2

sum e2 if test==1

scalar esum= `r(sum)'/`r(N)'

scalar model1_RMSE= esum^.5

display model1_RMSE Variable | Obs Mean Std. Dev. Min Max

-------------+---------------------------------------------------------

e2 | 7 .3319141 .1891047 .0326187 .5083123

.57611988Mean Absolute Error (MAE)

Calculate MAE for AR(1) model

gen e_abs = abs(e) if test ==1

sum e_abs if test==1

scalar model1_MAE=`r(mean)'

display model1_MAE(49 missing values generated)

Variable | Obs Mean Std. Dev. Min Max

-------------+---------------------------------------------------------

e_abs | 7 .542014 .2109284 .1806064 .7129602

.542013992.2 One-Step Ahead VAR Model

One-step ahead we can use predict or forecast for VAR Model (lagged employment and lagged inflation)

Train the Model

Our predict command will produce the same results as forecast solve, static

Forecast for Model 2

One-Step-Ahead Forecast of VAR Model

Computing static forecasts for model forecast2.

-----------------------------------------------

Starting period: 1997

Ending period: 2003

Forecast prefix: st2_

1997: ............

1998: ...........

1999: ...........

2000: .............

2001: ..............

2002: .............

2003: ..............

Forecast 1 variable spanning 7 periods.

---------------------------------------

+------------------------------+

| year unem st2_unem |

|------------------------------|

50. | 1997 4.9000001 5.3484678 |

51. | 1998 4.5 4.896451 |

52. | 1999 4.1999998 4.5091372 |

53. | 2000 4 4.4251752 |

54. | 2001 4.8000002 4.5160618 |

|------------------------------|

55. | 2002 5.8000002 4.9235368 |

56. | 2003 6 5.3502712 |

+------------------------------+Dynamic Forecast of VAR Model

Computing dynamic forecasts for model forecast2.

------------------------------------------------

Starting period: 1997

Ending period: 2003

Forecast prefix: dy2_

1997: ............

1998: .............

1999: .............

2000: ............

2001: .............

2002: ............

2003: .............

Forecast 1 variable spanning 7 periods.

---------------------------------------

+------------------------------------------+

| year unem st2_unem dy2_unem |

|------------------------------------------|

50. | 1997 4.9000001 5.3484678 5.3484678 |

51. | 1998 4.5 4.896451 5.1866217 |

52. | 1999 4.1999998 4.5091372 4.9533992 |

53. | 2000 4 4.4251752 4.9126439 |

54. | 2001 4.8000002 4.5160618 5.1065664 |

|------------------------------------------|

55. | 2002 5.8000002 4.9235368 5.1218934 |

56. | 2003 6 5.3502712 4.9115181 |

+------------------------------------------+2.2.1 Calculate RMSE and MAE

Calculate RMSE for the VAR model

gen e = unem - st2_unem

gen e2 = e^2

sum e2 if test==1

scalar esum2 = `r(sum)'/`r(N)'

scalar model2_RMSE=esum2^.5

display model2_RMSE Variable | Obs Mean Std. Dev. Min Max

-------------+---------------------------------------------------------

e2 | 7 .2722276 .2459784 .080621 .7681881

.52175434Calculate MAE for VAR model

Variable | Obs Mean Std. Dev. Min Max

-------------+---------------------------------------------------------

e_abs | 7 .4841946 .2099534 .2839384 .8764634

.484194552.3 Compare AR(1) and VAR models

Which model do we use? The model that minimizes the error.

Compare Results with RMSE and MSE

display "Model 1: RMSE="model1_RMSE " and MAE="model1_MAE

display "Model 2: RMSE="model2_RMSE " and MAE="model1_MAE

display "Model 2 with lagged unemployment and lagged inflation has lower RMSE and MAE."Model 1: RMSE=.57611988 and MAE=.54201399

Model 2: RMSE=.52175434 and MAE=.48419455

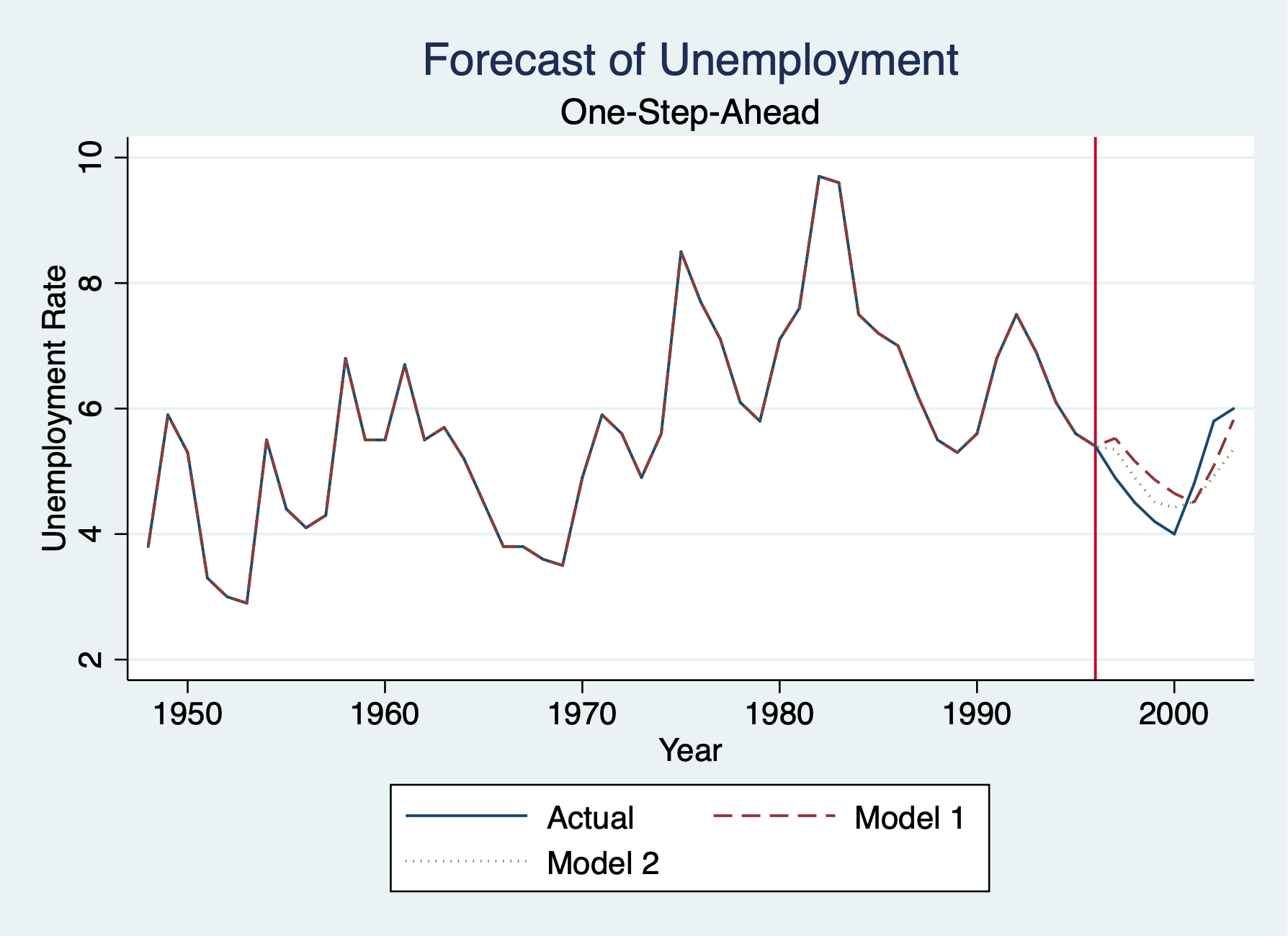

Model 2 with lagged unemployment and lagged inflation has lower RMSE and MAE.Graph the Forecasts

Forecasting Line

twoway line unem year || line st_unem year, lpattern(dash) || line st2_unem year, lpattern(dot) ///

title("Forecast of Unemployment") xtitle("Year") subtitle("One-Step-Ahead") ytitle("Unemployment Rate") xline(1996) ///

legend(order(1 "Actual" 2 "Model 1" 3 "Model 2"))

graph export "/Users/Sam/Desktop/Econ 645/Stata/week_11_forecast.png", replace