Chapter 1 Unit Roots

Lesson: when we have a unit root process or Time Series integrated of order one \(I(1)\) we can use a first difference to transform the time series into a weakly dependent and often stationary process.

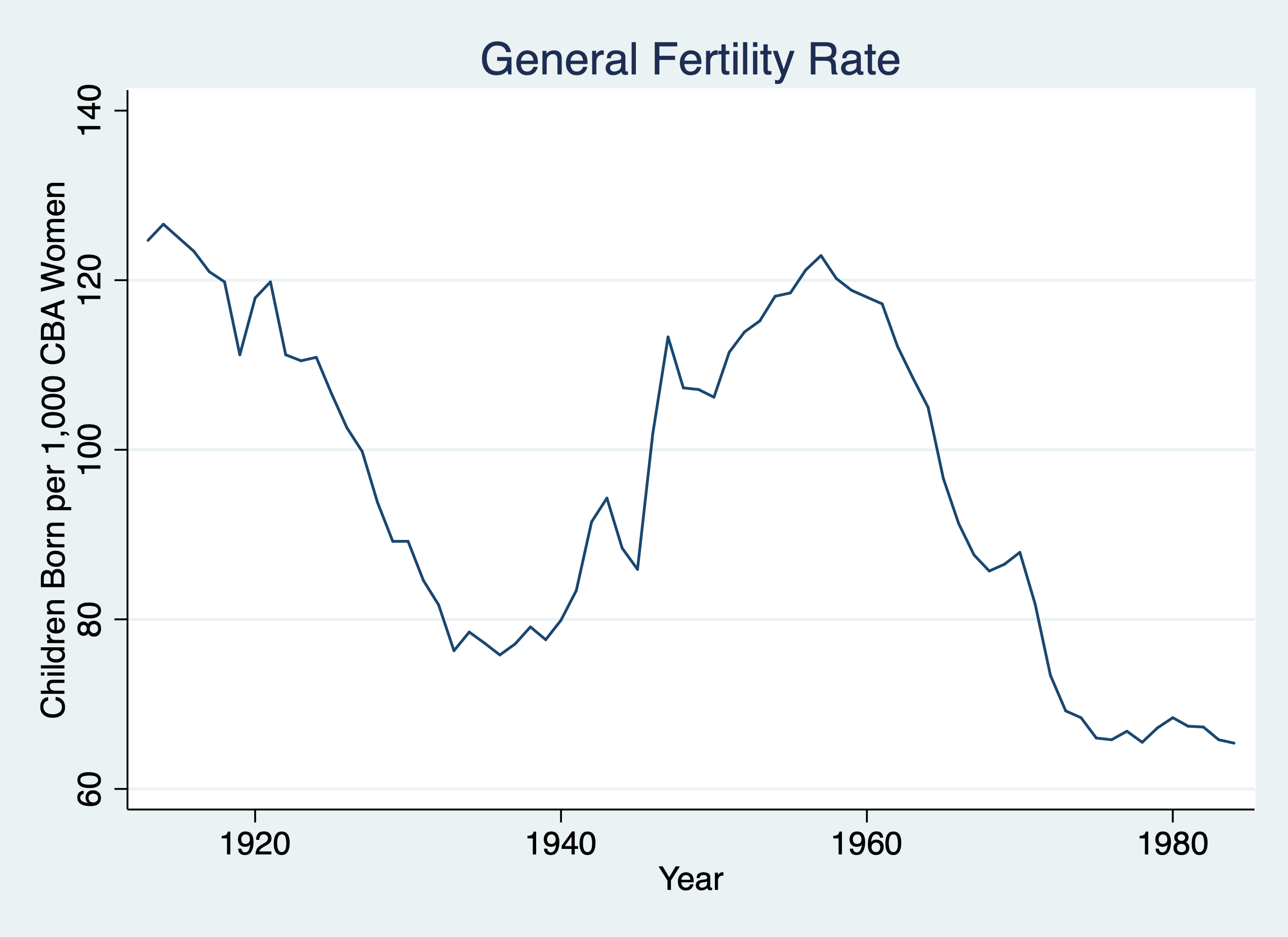

1.1 Example: Revisit Fertility

Set the time series

/Users/Sam/Desktop/Econ 645/Data/Wooldridge

time variable: year, 1913 to 1984

delta: 1 unitPlot the Graph

twoway line gfr year, title("General Fertility Rate") ytitle("Children Born per 1,000 CBA Women") xtitle("Year")

graph export "/Users/Sam/Desktop/Econ 645/Stata/week_11_i1.png", replace

Estimate autocorrelation or estimate \(\hat{\rho}\)

Source | SS df MS Number of obs = 71

-------------+---------------------------------- F(1, 69) = 1413.53

Model | 25734.824 1 25734.824 Prob > F = 0.0000

Residual | 1256.21904 69 18.2060731 R-squared = 0.9535

-------------+---------------------------------- Adj R-squared = 0.9528

Total | 26991.043 70 385.586329 Root MSE = 4.2669

------------------------------------------------------------------------------

gfr | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

gfr |

L1. | .9777202 .0260053 37.60 0.000 .925841 1.029599

|

_cons | 1.304937 2.548821 0.51 0.610 -3.779822 6.389695

------------------------------------------------------------------------------Our result is rho-hat is 0.98, which is indicative of a unit root process. Under our TS assumptions our t statistics are invalid, but if we use a transformation using a first-difference process, we can relax those assumptions under the TSC assumptions. If our \(I(1)\) becomes \(I(0)\), then our TSC assumptions are potentially valid.

First Difference both dependent and independent

Source | SS df MS Number of obs = 71

-------------+---------------------------------- F(1, 69) = 2.26

Model | 40.3237206 1 40.3237206 Prob > F = 0.1370

Residual | 1229.25866 69 17.8153428 R-squared = 0.0318

-------------+---------------------------------- Adj R-squared = 0.0177

Total | 1269.58238 70 18.1368911 Root MSE = 4.2208

------------------------------------------------------------------------------

D.gfr | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

pe |

D1. | -.0426776 .0283672 -1.50 0.137 -.0992686 .0139134

|

_cons | -.7847796 .5020398 -1.56 0.123 -1.786322 .2167625

------------------------------------------------------------------------------Our result is that the real value of the personal exemption is associated with a 0.043 decrease in fertility or a 23 dollar increase in the real value of the personal exemption is associated with a 1 child per capita (1,000 CBA Women). This is a bit unexpected, but still insignificant. Let’s add some lags.

First differnce with more than 1 lag

Source | SS df MS Number of obs = 69

-------------+---------------------------------- F(3, 65) = 6.56

Model | 293.259859 3 97.7532864 Prob > F = 0.0006

Residual | 968.199959 65 14.895384 R-squared = 0.2325

-------------+---------------------------------- Adj R-squared = 0.1971

Total | 1261.45982 68 18.5508797 Root MSE = 3.8595

------------------------------------------------------------------------------

D.gfr | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

pe |

D1. | -.0362021 .0267737 -1.35 0.181 -.089673 .0172687

|

pe_1 |

D1. | -.0139706 .0275539 -0.51 0.614 -.0689997 .0410584

|

pe_2 |

D1. | .1099896 .0268797 4.09 0.000 .0563071 .1636721

|

_cons | -.9636787 .4677599 -2.06 0.043 -1.89786 -.0294976

------------------------------------------------------------------------------Our results show that increases in the current and prior period real value personal exemption is not statistically significant. However, a 1 dollar increase in the real value of personal exemption is associated two period prior is associated with an increase of .110 child per capita (or $9.1 increase is associated with an increase of 1 child per capita.

1.2 Wages and Productivity

\(I(1)\) process with the presence of a linear trend

We want to estimate the elasticity of hourly wage with respect to output per hour (or labor productivity).

\[ ln(hrwage_t)=\beta_0 + \beta_1 ln(outphr_t) + \beta_2 t + u_t \]

Set Time Series and estimate the contemporaneous model

cd "/Users/Sam/Desktop/Econ 645/Data/Wooldridge"

use earns.dta, clear

tsset year, yearly

reg lhrwage loutphr t/Users/Sam/Desktop/Econ 645/Data/Wooldridge

time variable: year, 1947 to 1987

delta: 1 year

Source | SS df MS Number of obs = 41

-------------+---------------------------------- F(2, 38) = 641.22

Model | 1.04458064 2 .522290318 Prob > F = 0.0000

Residual | .030951776 38 .00081452 R-squared = 0.9712

-------------+---------------------------------- Adj R-squared = 0.9697

Total | 1.07553241 40 .02688831 Root MSE = .02854

------------------------------------------------------------------------------

lhrwage | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

loutphr | 1.639639 .0933471 17.56 0.000 1.450668 1.828611

t | -.01823 .0017482 -10.43 0.000 -.021769 -.0146909

_cons | -5.328454 .3744492 -14.23 0.000 -6.086487 -4.570421

------------------------------------------------------------------------------We estimate that the elasticity is very large, where a 1% increase in labor productivity (output per hour) is associated with a 1.64% increase in hourly wage. Let’s test for autocorrelation with accounting for the linear trend.

Source | SS df MS Number of obs = 40

-------------+---------------------------------- F(2, 37) = 1595.37

Model | .921760671 2 .460880336 Prob > F = 0.0000

Residual | .010688817 37 .000288887 R-squared = 0.9885

-------------+---------------------------------- Adj R-squared = 0.9879

Total | .932449488 39 .023908961 Root MSE = .017

------------------------------------------------------------------------------

lhrwage | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

lhrwage |

L1. | .9842872 .0334331 29.44 0.000 .9165452 1.052029

|

t | -.0009039 .0004732 -1.91 0.064 -.0018626 .0000548

_cons | .0544169 .0413998 1.31 0.197 -.0294671 .1383008

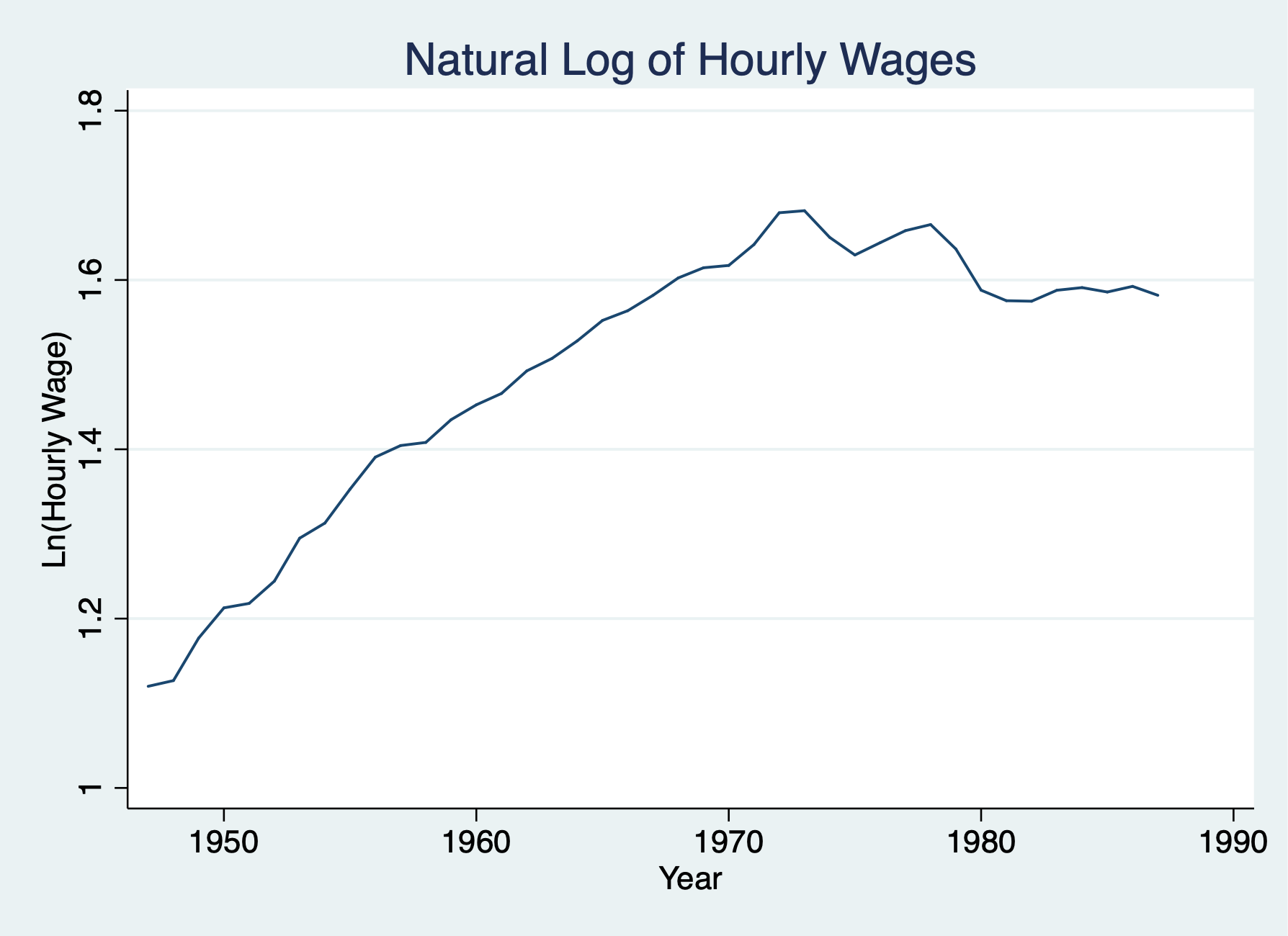

------------------------------------------------------------------------------We have some evidence for a unit root process, so we’ll use the first-difference to transform the I(1) process into a I(0) process. We’ll no longer need the time trend

twoway line lhrwage year, title("Natural Log of Hourly Wages") ytitle("Ln(Hourly Wage)") xtitle("Year")

graph export "/Users/Sam/Desktop/Econ 645/Stata/week_11_hrwage1.png", replace

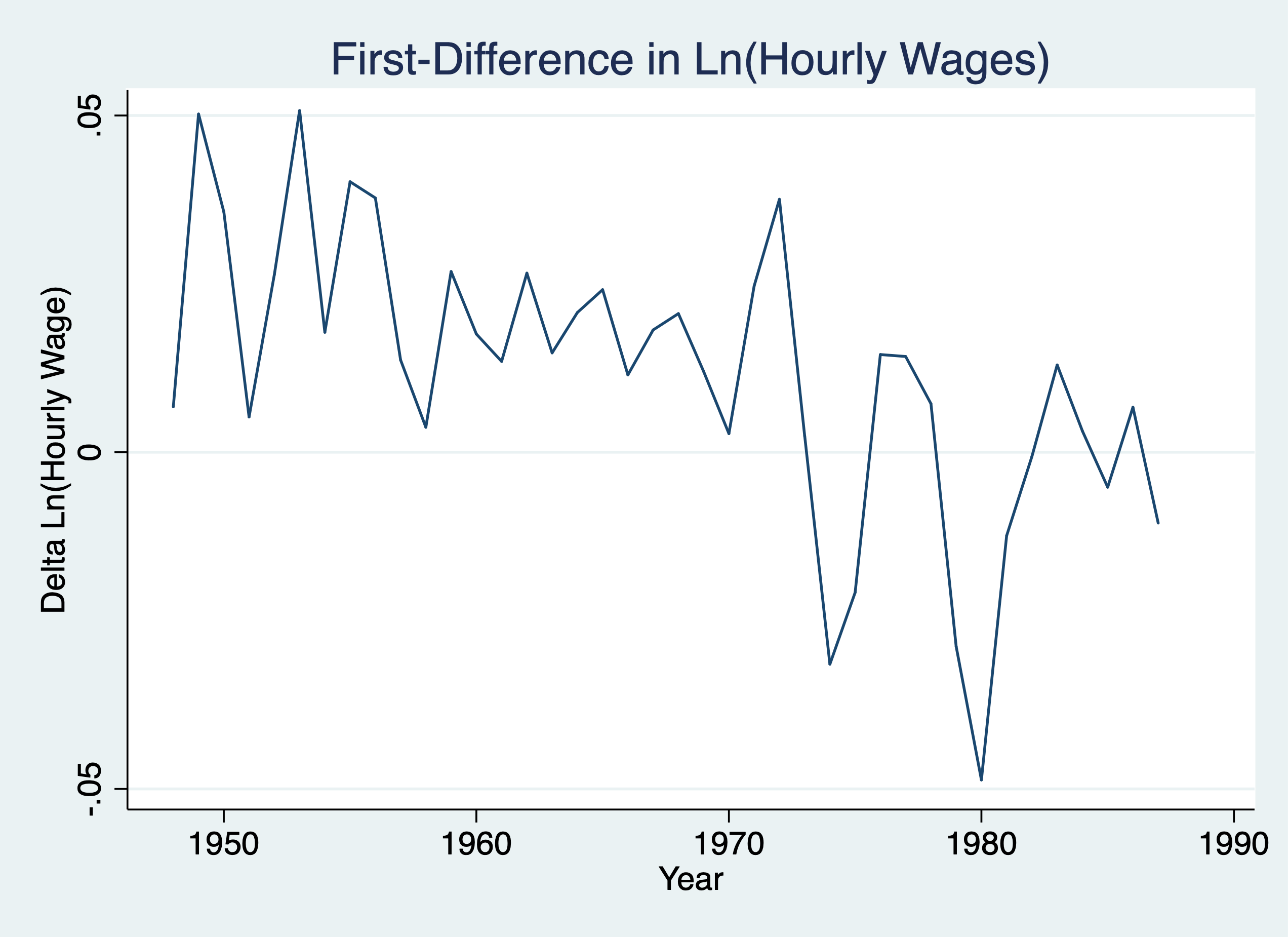

twoway line d.lhrwage year, title("First-Difference in Ln(Hourly Wages)") ytitle("Delta Ln(Hourly Wage)") xtitle("Year")

graph export "/Users/Sam/Desktop/Econ 645/Stata/week_11_hrwage2.png", replace

We’ll keep the trend based upon our prior graph

Source | SS df MS Number of obs = 40

-------------+---------------------------------- F(2, 37) = 19.12

Model | .008727211 2 .004363605 Prob > F = 0.0000

Residual | .008445792 37 .000228265 R-squared = 0.5082

-------------+---------------------------------- Adj R-squared = 0.4816

Total | .017173003 39 .000440333 Root MSE = .01511

------------------------------------------------------------------------------

D.lhrwage | Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

loutphr |

D1. | .5511404 .1733698 3.18 0.003 .1998598 .9024209

|

t | -.0007637 .0002321 -3.29 0.002 -.0012339 -.0002935

_cons | .0176094 .0074784 2.35 0.024 .0024567 .0327622

------------------------------------------------------------------------------Our transformed model shows that a 1% increase in output per hour is associated with a .55% increase in hourly wage.