. clear . set more off

Set Working Directory

. cd "/Users/Sam/Desktop/Econ 645/Data/Wooldridge" /Users/Sam/Desktop/Econ 645/Data/Wooldridge

. use fertil3.dta, clear

Set Time Series

. tsset year

time variable: year, 1913 to 1984

delta: 1 unit

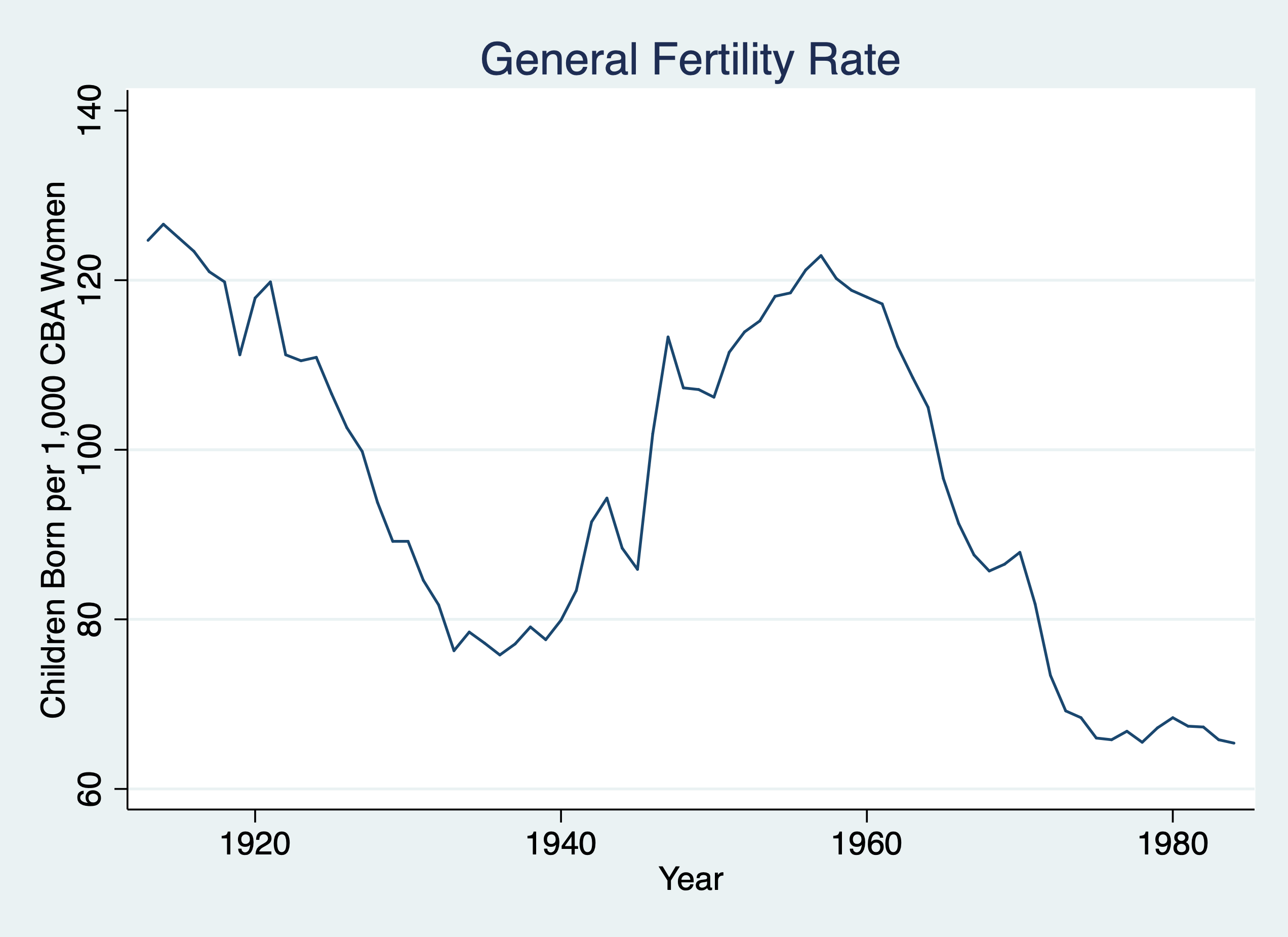

. twoway line gfr year, title("General Fertility Rate") ytitle("Children Born per 1,000 CBA Women") xtitle("Year")

. graph export "/Users/Sam/Desktop/Econ 645/Stata/week_11_i1.png", replace

(file /Users/Sam/Desktop/Econ 645/Stata/week_11_i1.png written in PNG format)

Estimate autocorrelation or estimate rho-hat

. reg gfr l.gfr

Source │ SS df MS Number of obs = 71

─────────────┼────────────────────────────────── F(1, 69) = 1413.53

Model │ 25734.824 1 25734.824 Prob > F = 0.0000

Residual │ 1256.21904 69 18.2060731 R-squared = 0.9535

─────────────┼────────────────────────────────── Adj R-squared = 0.9528

Total │ 26991.043 70 385.586329 Root MSE = 4.2669

─────────────┬────────────────────────────────────────────────────────────────

gfr │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

gfr │

L1. │ .9777202 .0260053 37.60 0.000 .925841 1.029599

│

_cons │ 1.304937 2.548821 0.51 0.610 -3.779822 6.389695

─────────────┴────────────────────────────────────────────────────────────────

Our result is rho-hat is 0.98, which is indicative of a unit root process. Under our TS assumptions our t statistics are invalid, but if we use a transformation using a first-difference process, we can relax those assumptions under the TSC assumptions. If our I(1) becomes I(0), then our TSC assumptions are potentially valid.

First Difference both dependent and independent

. reg d.gfr d.pe if year < 1985

Source │ SS df MS Number of obs = 71

─────────────┼────────────────────────────────── F(1, 69) = 2.26

Model │ 40.3237206 1 40.3237206 Prob > F = 0.1370

Residual │ 1229.25866 69 17.8153428 R-squared = 0.0318

─────────────┼────────────────────────────────── Adj R-squared = 0.0177

Total │ 1269.58238 70 18.1368911 Root MSE = 4.2208

─────────────┬────────────────────────────────────────────────────────────────

D.gfr │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

pe │

D1. │ -.0426776 .0283672 -1.50 0.137 -.0992686 .0139134

│

_cons │ -.7847796 .5020398 -1.56 0.123 -1.786322 .2167625

─────────────┴────────────────────────────────────────────────────────────────

Our result is that the real value of the personal exemption is associated with a 0.043 decrease in fertility or a 23 dollar increase in the real value of the personal exemption is associated with a 1 child per capita (1,000 CBA Women). This is a bit unexpected, but still insignificant. Let’s add some lags.

First differnce with more than 1 lag

. reg d.gfr d.pe d.pe_1 d.pe_2 if year < 1985

Source │ SS df MS Number of obs = 69

─────────────┼────────────────────────────────── F(3, 65) = 6.56

Model │ 293.259859 3 97.7532864 Prob > F = 0.0006

Residual │ 968.199959 65 14.895384 R-squared = 0.2325

─────────────┼────────────────────────────────── Adj R-squared = 0.1971

Total │ 1261.45982 68 18.5508797 Root MSE = 3.8595

─────────────┬────────────────────────────────────────────────────────────────

D.gfr │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

pe │

D1. │ -.0362021 .0267737 -1.35 0.181 -.089673 .0172687

│

pe_1 │

D1. │ -.0139706 .0275539 -0.51 0.614 -.0689997 .0410584

│

pe_2 │

D1. │ .1099896 .0268797 4.09 0.000 .0563071 .1636721

│

_cons │ -.9636787 .4677599 -2.06 0.043 -1.89786 -.0294976

─────────────┴────────────────────────────────────────────────────────────────

Our results show that increases in the current and prior period real value personal exemption is not statistically significant. However, a 1 dollar increase in the real value of personal exemption is associated two period prior is associated with an increase of .110 child per capita (or $9.1 increase is associated with an increase of 1 child per capita.

I(1) process with the presence of a linear trend

. use earns.dta, clear

Set Time Series

. tsset year, yearly

time variable: year, 1947 to 1987

delta: 1 year

We want to estimate the elasticity of hourly wage with respect to output per hour (or labor productivity). \[ ln(hrwage_t)=\beta_0 + \beta_1 ln(outphr_t) + \beta_2 t + u_t \]

We estimate the contemporaneous model

. reg lhrwage loutphr t

Source │ SS df MS Number of obs = 41

─────────────┼────────────────────────────────── F(2, 38) = 641.22

Model │ 1.04458064 2 .522290318 Prob > F = 0.0000

Residual │ .030951776 38 .00081452 R-squared = 0.9712

─────────────┼────────────────────────────────── Adj R-squared = 0.9697

Total │ 1.07553241 40 .02688831 Root MSE = .02854

─────────────┬────────────────────────────────────────────────────────────────

lhrwage │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

loutphr │ 1.639639 .0933471 17.56 0.000 1.450668 1.828611

t │ -.01823 .0017482 -10.43 0.000 -.021769 -.0146909

_cons │ -5.328454 .3744492 -14.23 0.000 -6.086487 -4.570421

─────────────┴────────────────────────────────────────────────────────────────

We estimate that the elasticity is very large, where a 1% increase in labor productivity (output per hour) is associated with a 1.64% increase in hourly wage. Let’s test for autocorrelation with accounting for the linear trend.

. reg lhrwage l.lhrwage t

Source │ SS df MS Number of obs = 40

─────────────┼────────────────────────────────── F(2, 37) = 1595.37

Model │ .921760671 2 .460880336 Prob > F = 0.0000

Residual │ .010688817 37 .000288887 R-squared = 0.9885

─────────────┼────────────────────────────────── Adj R-squared = 0.9879

Total │ .932449488 39 .023908961 Root MSE = .017

─────────────┬────────────────────────────────────────────────────────────────

lhrwage │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lhrwage │

L1. │ .9842872 .0334331 29.44 0.000 .9165452 1.052029

│

t │ -.0009039 .0004732 -1.91 0.064 -.0018626 .0000548

_cons │ .0544169 .0413998 1.31 0.197 -.0294671 .1383008

─────────────┴────────────────────────────────────────────────────────────────

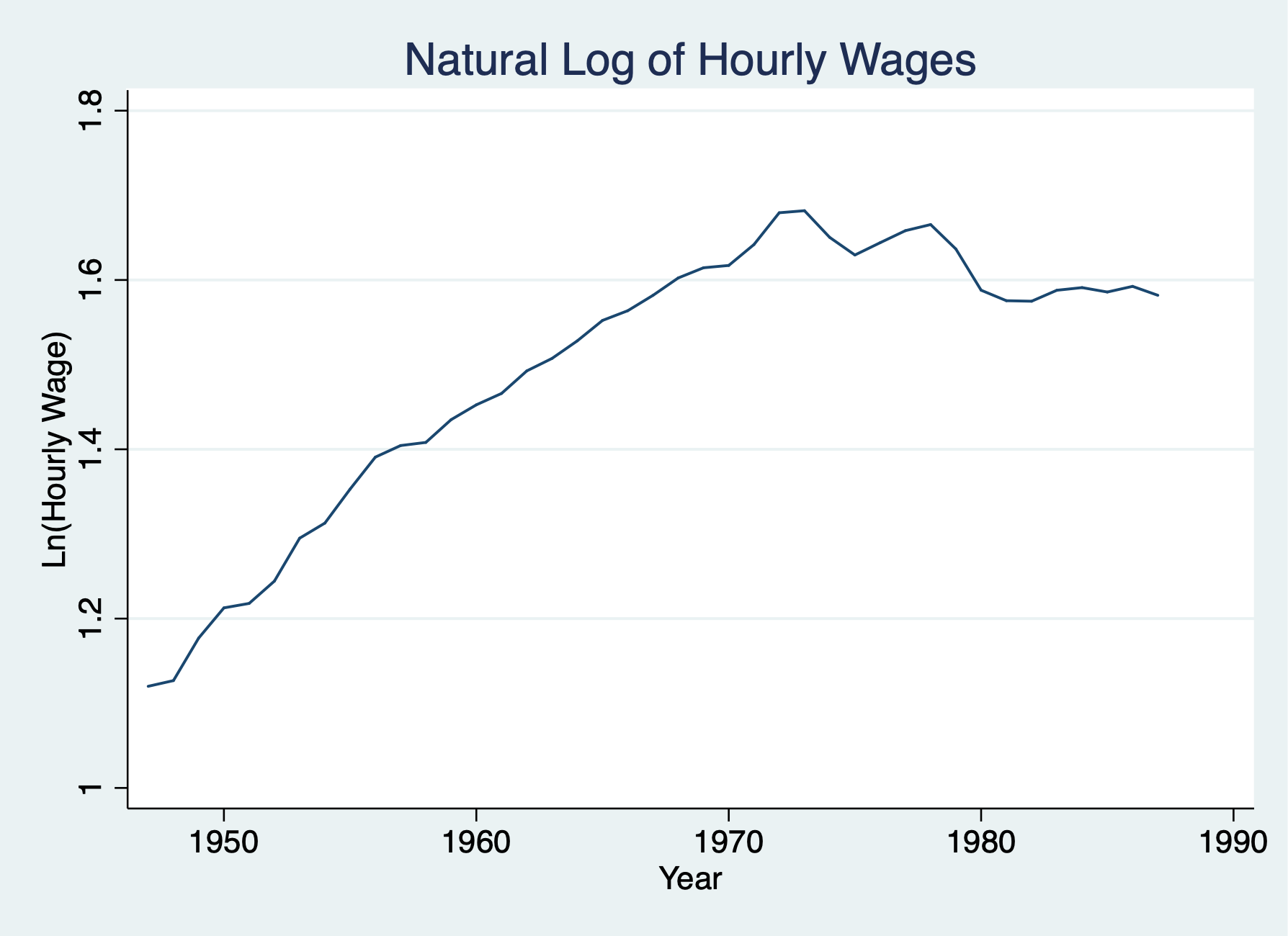

We have some evidence for a unit root process, so we’ll use the first-difference to transform the I(1) process into a I(0) process. We’ll no longer need the time trend

. twoway line lhrwage year, title("Natural Log of Hourly Wages") ytitle("Ln(Hourly Wage)") xtitle("Year")

. graph export "/Users/Sam/Desktop/Econ 645/Stata/week_11_hrwage1.png", replace

(file /Users/Sam/Desktop/Econ 645/Stata/week_11_hrwage1.png written in PNG format)

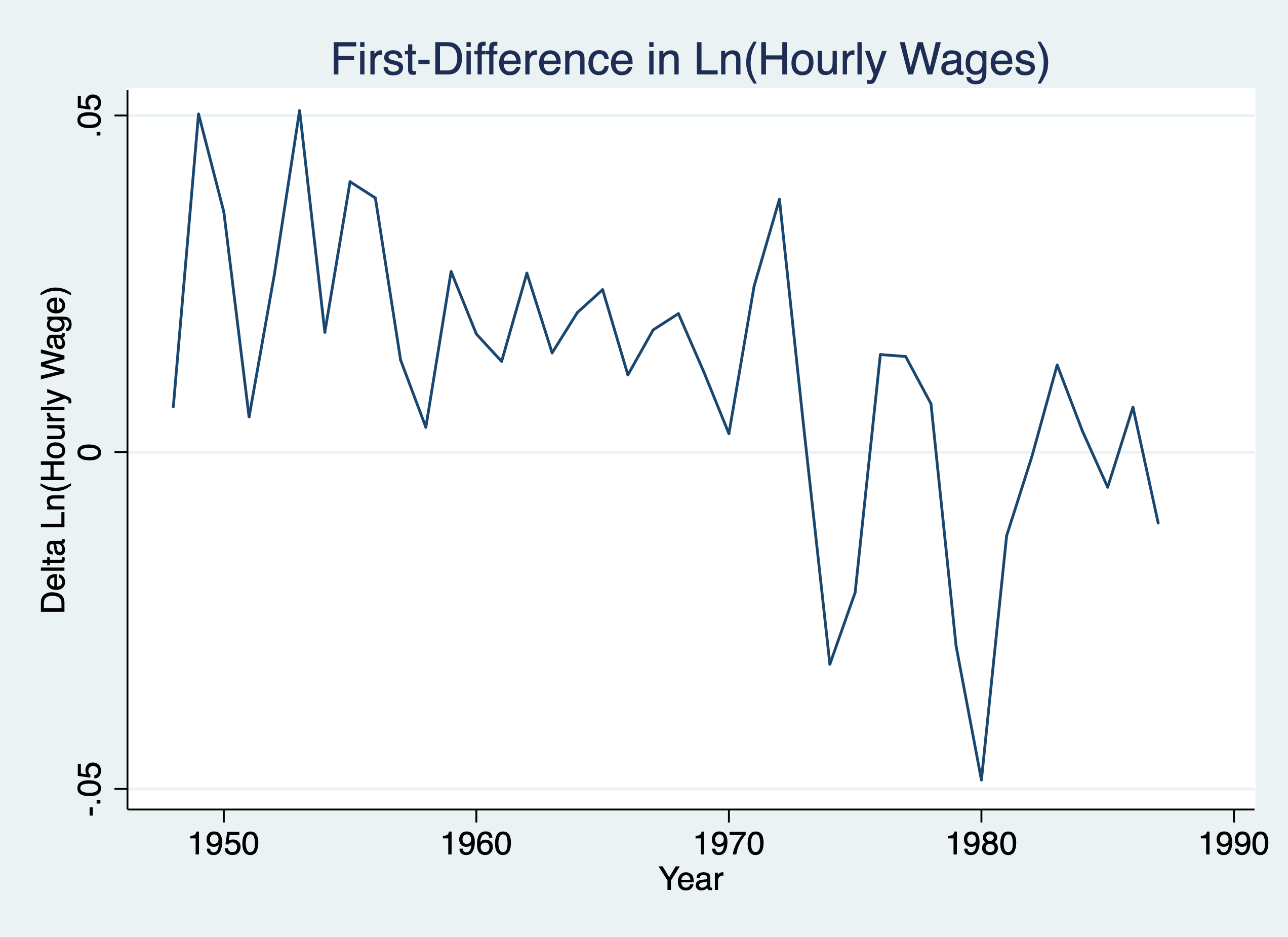

. twoway line d.lhrwage year, title("First-Difference in Ln(Hourly Wages)") ytitle("Delta Ln(Hourly Wage)") xtitle(

> "Year")

. graph export "/Users/Sam/Desktop/Econ 645/Stata/week_11_hrwage2.png", replace

(file /Users/Sam/Desktop/Econ 645/Stata/week_11_hrwage2.png written in PNG format)

We’ll keep the trend based upon our prior graph

. reg d.lhrwage d.loutphr t

Source │ SS df MS Number of obs = 40

─────────────┼────────────────────────────────── F(2, 37) = 19.12

Model │ .008727211 2 .004363605 Prob > F = 0.0000

Residual │ .008445792 37 .000228265 R-squared = 0.5082

─────────────┼────────────────────────────────── Adj R-squared = 0.4816

Total │ .017173003 39 .000440333 Root MSE = .01511

─────────────┬────────────────────────────────────────────────────────────────

D.lhrwage │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

loutphr │

D1. │ .5511404 .1733698 3.18 0.003 .1998598 .9024209

│

t │ -.0007637 .0002321 -3.29 0.002 -.0012339 -.0002935

_cons │ .0176094 .0074784 2.35 0.024 .0024567 .0327622

─────────────┴────────────────────────────────────────────────────────────────

Our transformed model shows that a 1% increase in output per hour is associated with a .55% increase in hourly wage.

. use fertil3.dta

Set Time Series

. tsset year, yearly

time variable: year, 1913 to 1984

delta: 1 year

We’ll estimate a Finite Distributed Lag model for the first difference of general fertility onto the first difference of personal exemptions. If our model is dynamically complete, then no additional lags of gfr or pe are needed.

Our First-difference model with one lag of pe

. reg d.gfr d.pe d.pe_1 if year < 1985

Source │ SS df MS Number of obs = 70

─────────────┼────────────────────────────────── F(2, 67) = 1.20

Model │ 43.7985353 2 21.8992676 Prob > F = 0.3063

Residual │ 1218.19557 67 18.1820235 R-squared = 0.0347

─────────────┼────────────────────────────────── Adj R-squared = 0.0059

Total │ 1261.99411 69 18.2897697 Root MSE = 4.264

─────────────┬────────────────────────────────────────────────────────────────

D.gfr │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

pe │

D1. │ -.0456497 .0294689 -1.55 0.126 -.1044699 .0131704

│

pe_1 │

D1. │ .0134149 .0295326 0.45 0.651 -.0455324 .0723623

│

_cons │ -.8372962 .5117337 -1.64 0.106 -1.858721 .1841286

─────────────┴────────────────────────────────────────────────────────────────

Is this dynamically complete? Let’s add a second lag of pe

. reg d.gfr d.pe d.pe_1 d.pe_2 if year < 1985

Source │ SS df MS Number of obs = 69

─────────────┼────────────────────────────────── F(3, 65) = 6.56

Model │ 293.259859 3 97.7532864 Prob > F = 0.0006

Residual │ 968.199959 65 14.895384 R-squared = 0.2325

─────────────┼────────────────────────────────── Adj R-squared = 0.1971

Total │ 1261.45982 68 18.5508797 Root MSE = 3.8595

─────────────┬────────────────────────────────────────────────────────────────

D.gfr │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

pe │

D1. │ -.0362021 .0267737 -1.35 0.181 -.089673 .0172687

│

pe_1 │

D1. │ -.0139706 .0275539 -0.51 0.614 -.0689997 .0410584

│

pe_2 │

D1. │ .1099896 .0268797 4.09 0.000 .0563071 .1636721

│

_cons │ -.9636787 .4677599 -2.06 0.043 -1.89786 -.0294976

─────────────┴────────────────────────────────────────────────────────────────

Add lag of d.gfr and see it wasn’t dynamically complete

. reg d.gfr d.gfr_1 d.pe d.pe_1 d.pe_2 if year < 1985

Source │ SS df MS Number of obs = 69

─────────────┼────────────────────────────────── F(4, 64) = 7.46

Model │ 401.286162 4 100.32154 Prob > F = 0.0001

Residual │ 860.173657 64 13.4402134 R-squared = 0.3181

─────────────┼────────────────────────────────── Adj R-squared = 0.2755

Total │ 1261.45982 68 18.5508797 Root MSE = 3.6661

─────────────┬────────────────────────────────────────────────────────────────

D.gfr │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

gfr_1 │

D1. │ .3002422 .1059034 2.84 0.006 .0886758 .5118086

│

pe │

D1. │ -.0454721 .0256417 -1.77 0.081 -.0966972 .005753

│

pe_1 │

D1. │ .002064 .0267776 0.08 0.939 -.0514303 .0555584

│

pe_2 │

D1. │ .1051346 .0255904 4.11 0.000 .054012 .1562572

│

_cons │ -.7021594 .4537988 -1.55 0.127 -1.608727 .2044079

─────────────┴────────────────────────────────────────────────────────────────

We’ll use our t-test for serial correlation with strictly exogenous regressors under the assumption that our regressors are exogenous.

. use phillips.dta, clear

Set Time Series

. tsset year, yearly

time variable: year, 1948 to 2003

delta: 1 year

We estimated a static Phillips Curve and an augmented Phillips Curve last week. We’ll retest the models for serial correlation.

Test for serial correlation in Static Model Noticeable serial correlation

. reg inf unem if year < 1997

Source │ SS df MS Number of obs = 49

─────────────┼────────────────────────────────── F(1, 47) = 2.62

Model │ 25.6369575 1 25.6369575 Prob > F = 0.1125

Residual │ 460.61979 47 9.80042107 R-squared = 0.0527

─────────────┼────────────────────────────────── Adj R-squared = 0.0326

Total │ 486.256748 48 10.1303489 Root MSE = 3.1306

─────────────┬────────────────────────────────────────────────────────────────

inf │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

unem │ .4676257 .2891262 1.62 0.112 -.1140213 1.049273

_cons │ 1.42361 1.719015 0.83 0.412 -2.034602 4.881822

─────────────┴────────────────────────────────────────────────────────────────

Breusch-Godfrey Test

. estat bgodfrey

Breusch-Godfrey LM test for autocorrelation

─────────────┬─────────────────────────────────────────────────────────────

lags(p) │ chi2 df Prob > chi2

─────────────┼─────────────────────────────────────────────────────────────

1 │ 18.472 1 0.0000

─────────────┴─────────────────────────────────────────────────────────────

H0: no serial correlation

Simple AR(1) test

. predict u, resid

. reg u l.u, noconst

Source │ SS df MS Number of obs = 55

─────────────┼────────────────────────────────── F(1, 54) = 29.61

Model │ 161.010846 1 161.010846 Prob > F = 0.0000

Residual │ 293.652171 54 5.43800317 R-squared = 0.3541

─────────────┼────────────────────────────────── Adj R-squared = 0.3422

Total │ 454.663017 55 8.26660031 Root MSE = 2.332

─────────────┬────────────────────────────────────────────────────────────────

u │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

u │

L1. │ .5822453 .1070035 5.44 0.000 .3677161 .7967745

─────────────┴────────────────────────────────────────────────────────────────

Test for serial correlation in Augmented Serial correlation is removed with the first-difference in inflation

. reg d.inf unem if year < 1997

Source │ SS df MS Number of obs = 48

─────────────┼────────────────────────────────── F(1, 46) = 5.56

Model │ 33.3829996 1 33.3829996 Prob > F = 0.0227

Residual │ 276.305138 46 6.00663344 R-squared = 0.1078

─────────────┼────────────────────────────────── Adj R-squared = 0.0884

Total │ 309.688138 47 6.58910932 Root MSE = 2.4508

─────────────┬────────────────────────────────────────────────────────────────

D.inf │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

unem │ -.5425869 .2301559 -2.36 0.023 -1.005867 -.079307

_cons │ 3.030581 1.37681 2.20 0.033 .259206 5.801955

─────────────┴────────────────────────────────────────────────────────────────

. predict u2, resid

(1 missing value generated)

Breusch-Godfrey Test

. estat bgodfrey

Breusch-Godfrey LM test for autocorrelation

─────────────┬─────────────────────────────────────────────────────────────

lags(p) │ chi2 df Prob > chi2

─────────────┼─────────────────────────────────────────────────────────────

1 │ 0.062 1 0.8039

─────────────┴─────────────────────────────────────────────────────────────

H0: no serial correlation

Durban-Watson Test

. estat dwatson Durbin-Watson d-statistic( 2, 48) = 1.769648

\[ d_L = 1.503 \] \[ d_U = 1.585 \] \[ 1.769648 > 1.585 \] We fail to reject the null hypothesis.

AR(1) Test

. reg u2 l.u2, noconst

Source │ SS df MS Number of obs = 54

─────────────┼────────────────────────────────── F(1, 53) = 0.07

Model │ .267251656 1 .267251656 Prob > F = 0.7905

Residual │ 198.724905 53 3.74952651 R-squared = 0.0013

─────────────┼────────────────────────────────── Adj R-squared = -0.0175

Total │ 198.992157 54 3.68503994 Root MSE = 1.9364

─────────────┬────────────────────────────────────────────────────────────────

u2 │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

u2 │

L1. │ -.0308131 .1154154 -0.27 0.791 -.262307 .2006808

─────────────┴────────────────────────────────────────────────────────────────

Test change in error terms for FD assumption on serial correlation so that the differences in errors are not correlated.

. gen u2_1=l.u2 (2 missing values generated)

. reg d.u2 d.u2_1, noconst

Source │ SS df MS Number of obs = 53

─────────────┼────────────────────────────────── F(1, 52) = 2.01

Model │ 13.6239993 1 13.6239993 Prob > F = 0.1623

Residual │ 352.532902 52 6.77947888 R-squared = 0.0372

─────────────┼────────────────────────────────── Adj R-squared = 0.0187

Total │ 366.156901 53 6.90862078 Root MSE = 2.6037

─────────────┬────────────────────────────────────────────────────────────────

D.u2 │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

u2_1 │

D1. │ -.1661051 .1171734 -1.42 0.162 -.4012307 .0690204

─────────────┴────────────────────────────────────────────────────────────────

drop u u2

We fail to reject the null hypothesis that there is no serial correlation in the difference in error term.

Let’s add a lag in inflation to change our static model into a FDL model. We can also use the estat dwatson or dwstat

. reg inf l.inf unem if year < 1997

Source │ SS df MS Number of obs = 48

─────────────┼────────────────────────────────── F(2, 45) = 19.72

Model │ 219.518187 2 109.759094 Prob > F = 0.0000

Residual │ 250.471823 45 5.56604051 R-squared = 0.4671

─────────────┼────────────────────────────────── Adj R-squared = 0.4434

Total │ 469.99001 47 9.99978744 Root MSE = 2.3592

─────────────┬────────────────────────────────────────────────────────────────

inf │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

inf │

L1. │ .7278693 .1263167 5.76 0.000 .4734544 .9822841

│

unem │ -.2443814 .26124 -0.94 0.355 -.7705457 .2817829

_cons │ 2.43082 1.354276 1.79 0.079 -.2968325 5.158473

─────────────┴────────────────────────────────────────────────────────────────

. estat dwatson

Durbin-Watson d-statistic( 3, 48) = 1.477467

Or

. dwstat Durbin-Watson d-statistic( 3, 48) = 1.477467

First, let’s find our critical values:

https://www3.nd.edu/~wevans1/econ30331/Durbin_Watson_tables.pdf.

\[ DW(3,48)=1.48 \] and \[ d_L \approx 1.4 \] and \[ d_U \approx 1.67 \] so our DW test is

inconclusive. We’ll look at Durban-Watson and DW Tables again a bit

later.

Durban’s alternative statistic

. use prminwge, clear

Set Time Series

. tsset year

time variable: year, 1950 to 1987

delta: 1 unit

We’ll rerun our static model and regress the natural log of the employment-population ratio onto the natural log of the importance of minimum wage, the natural log of Puerto Rican Gross National Product, the natural log of US GNP, and a time trend.

. reg lprepop lmincov lprgnp lusgnp t if year < 1988

Source │ SS df MS Number of obs = 38

─────────────┼────────────────────────────────── F(4, 33) = 66.23

Model │ .284430187 4 .071107547 Prob > F = 0.0000

Residual │ .035428331 33 .001073586 R-squared = 0.8892

─────────────┼────────────────────────────────── Adj R-squared = 0.8758

Total │ .319858518 37 .008644825 Root MSE = .03277

─────────────┬────────────────────────────────────────────────────────────────

lprepop │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lmincov │ -.2122612 .0401524 -5.29 0.000 -.2939518 -.1305706

lprgnp │ .2852386 .0804922 3.54 0.001 .121476 .4490012

lusgnp │ .4860463 .2219829 2.19 0.036 .0344188 .9376739

t │ -.0266633 .0046267 -5.76 0.000 -.0360765 -.0172502

_cons │ -6.663432 1.257831 -5.30 0.000 -9.222508 -4.104356

─────────────┴────────────────────────────────────────────────────────────────

. predict u, resid

Test Serial Correlation with Durbin’s alternative statistic, which is valid when we don’t have strictly exogenous regressors.

. reg u l.u lmincov lprgnp lusgnp t, noconst

Source │ SS df MS Number of obs = 37

─────────────┼────────────────────────────────── F(5, 32) = 1.92

Model │ .007182064 5 .001436413 Prob > F = 0.1191

Residual │ .023990478 32 .000749702 R-squared = 0.2304

─────────────┼────────────────────────────────── Adj R-squared = 0.1101

Total │ .031172542 37 .000842501 Root MSE = .02738

─────────────┬────────────────────────────────────────────────────────────────

u │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

u │

L1. │ .4757945 .1653074 2.88 0.007 .1390742 .8125147

│

lmincov │ .041425 .0346345 1.20 0.240 -.0291232 .1119732

lprgnp │ -.0522061 .0615544 -0.85 0.403 -.1775883 .0731762

lusgnp │ .0606233 .0644769 0.94 0.354 -.070712 .1919585

t │ -.0005264 .0015194 -0.35 0.731 -.0036213 .0025685

─────────────┴────────────────────────────────────────────────────────────────

We can see that we reject the null hypothesis, since our rho-hat is 0.48 and statistically significant.

. use barium.dta, clear

Set Time Series

. tsset t, monthly

time variable: t, 1960m2 to 1970m12

delta: 1 month

We’ll look at our barium chloride model again to see if ITC complaints affect behavior of foreign exporters. We may have higher order of serial correlation since we are using monthly data.

. reg lchnimp lchempi lgas lrtwex befile6 affile6 afdec6

Source │ SS df MS Number of obs = 131

─────────────┼────────────────────────────────── F(6, 124) = 9.06

Model │ 19.4051607 6 3.23419346 Prob > F = 0.0000

Residual │ 44.2470875 124 .356831351 R-squared = 0.3049

─────────────┼────────────────────────────────── Adj R-squared = 0.2712

Total │ 63.6522483 130 .489632679 Root MSE = .59735

─────────────┬────────────────────────────────────────────────────────────────

lchnimp │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lchempi │ 3.117193 .4792021 6.50 0.000 2.168718 4.065668

lgas │ .1963504 .9066172 0.22 0.829 -1.598099 1.9908

lrtwex │ .9830183 .4001537 2.46 0.015 .1910022 1.775034

befile6 │ .0595739 .2609699 0.23 0.820 -.4569585 .5761064

affile6 │ -.0324064 .2642973 -0.12 0.903 -.5555249 .490712

afdec6 │ -.565245 .2858352 -1.98 0.050 -1.130993 .0005028

_cons │ -17.803 21.04537 -0.85 0.399 -59.45769 23.85169

─────────────┴────────────────────────────────────────────────────────────────

. predict u, resid

Test for p1=p2=p3=0 jointly with an F-test.

. reg u l.u l2.u l3.u lchempi lgas lrtwex befile6 affile6 afdec6, noconst

Source │ SS df MS Number of obs = 128

─────────────┼────────────────────────────────── F(9, 119) = 1.67

Model │ 4.8836741 9 .542630456 Prob > F = 0.1024

Residual │ 38.5511192 119 .323958985 R-squared = 0.1124

─────────────┼────────────────────────────────── Adj R-squared = 0.0453

Total │ 43.4347933 128 .339334323 Root MSE = .56917

─────────────┬────────────────────────────────────────────────────────────────

u │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

u │

L1. │ .215573 .0910635 2.37 0.020 .0352581 .3958878

L2. │ .1296804 .0917465 1.41 0.160 -.0519868 .3113477

L3. │ .1209405 .0906816 1.33 0.185 -.0586181 .3004992

│

lchempi │ -.105758 .4679356 -0.23 0.822 -1.032317 .8208012

lgas │ .0125667 .1187882 0.11 0.916 -.2226459 .2477792

lrtwex │ .0518992 .3452261 0.15 0.881 -.631683 .7354815

befile6 │ -.0730016 .249775 -0.29 0.771 -.567581 .4215779

affile6 │ -.122359 .2541453 -0.48 0.631 -.6255919 .380874

afdec6 │ -.0694522 .2737453 -0.25 0.800 -.6114953 .4725909

─────────────┴────────────────────────────────────────────────────────────────

Our reject the null hypothesis that all of the lags are equal to zero using an F-test.

. test l.u l2.u l3.u

( 1) L.u = 0

( 2) L2.u = 0

( 3) L3.u = 0

F( 3, 119) = 4.98

Prob > F = 0.0027

However, when we test our last two lags, they are jointly insignificant.

. test l2.u l3.u

( 1) L2.u = 0

( 2) L3.u = 0

F( 2, 119) = 2.42

Prob > F = 0.0930

. drop u

We have evidence of at least serial correlation to the order of one.

. use barium.dta, clear

Set Time Series

. tsset t, monthly

time variable: t, 1960m2 to 1970m12

delta: 1 month

. est clear

OLS

. eststo OLS: reg lchnimp lchempi lgas lrtwex befile6 affile6 afdec6

Source │ SS df MS Number of obs = 131

─────────────┼────────────────────────────────── F(6, 124) = 9.06

Model │ 19.4051607 6 3.23419346 Prob > F = 0.0000

Residual │ 44.2470875 124 .356831351 R-squared = 0.3049

─────────────┼────────────────────────────────── Adj R-squared = 0.2712

Total │ 63.6522483 130 .489632679 Root MSE = .59735

─────────────┬────────────────────────────────────────────────────────────────

lchnimp │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lchempi │ 3.117193 .4792021 6.50 0.000 2.168718 4.065668

lgas │ .1963504 .9066172 0.22 0.829 -1.598099 1.9908

lrtwex │ .9830183 .4001537 2.46 0.015 .1910022 1.775034

befile6 │ .0595739 .2609699 0.23 0.820 -.4569585 .5761064

affile6 │ -.0324064 .2642973 -0.12 0.903 -.5555249 .490712

afdec6 │ -.565245 .2858352 -1.98 0.050 -1.130993 .0005028

_cons │ -17.803 21.04537 -0.85 0.399 -59.45769 23.85169

─────────────┴────────────────────────────────────────────────────────────────

Prais-Winsten

. eststo Prais: prais lchnimp lchempi lgas lrtwex befile6 affile6 afdec6

Iteration 0: rho = 0.0000

Iteration 1: rho = 0.2708

Iteration 2: rho = 0.2910

Iteration 3: rho = 0.2930

Iteration 4: rho = 0.2932

Iteration 5: rho = 0.2932

Iteration 6: rho = 0.2932

Iteration 7: rho = 0.2932

Prais-Winsten AR(1) regression -- iterated estimates

Source │ SS df MS Number of obs = 131

─────────────┼────────────────────────────────── F(6, 124) = 5.24

Model │ 10.3252323 6 1.72087205 Prob > F = 0.0001

Residual │ 40.7593886 124 .328704747 R-squared = 0.2021

─────────────┼────────────────────────────────── Adj R-squared = 0.1635

Total │ 51.0846209 130 .392958622 Root MSE = .57333

─────────────┬────────────────────────────────────────────────────────────────

lchnimp │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lchempi │ 2.940949 .6328402 4.65 0.000 1.688381 4.193517

lgas │ 1.04638 .9773356 1.07 0.286 -.8880406 2.980801

lrtwex │ 1.132791 .5066578 2.24 0.027 .1299738 2.135609

befile6 │ -.0164787 .3193802 -0.05 0.959 -.6486216 .6156641

affile6 │ -.0331563 .3218101 -0.10 0.918 -.6701086 .603796

afdec6 │ -.5768122 .3419865 -1.69 0.094 -1.253699 .1000748

_cons │ -37.0777 22.7783 -1.63 0.106 -82.16235 8.006941

─────────────┼────────────────────────────────────────────────────────────────

rho │ .293217

─────────────┴────────────────────────────────────────────────────────────────

Durbin-Watson statistic (original) 1.458414

Durbin-Watson statistic (transformed) 2.087181

. predict u, resid

First, let’s find our critical values:

https://www3.nd.edu/~wevans1/econ30331/Durbin_Watson_tables.pdf.

For the OLS Estimator \[ DW(6,131) =

1.458414 \] For the Prasi-Winsten Estimator \[ DW(6,131) = 2.087181 \] and \[ d_L \approx 1.60 \] and \[ d_U \approx 1.81 \] We reject the null

hypothesis for the OLS estimator, but we fail to reject the null

hypothesis for the Prais-Winsten Estimator.

Our beta-hats in Prais-Winsten Estimator are similar to our OLS estimates, but our PW standard errors account for the serial correlation. Our OLS standard errors usually understate the actual sampling variation in the OLS estimators and should be treated with suspicion.

. esttab, mtitle se stat(N rho)

────────────────────────────────────────────

(1) (2)

OLS Prais

────────────────────────────────────────────

lchempi 3.117*** 2.941***

(0.479) (0.633)

lgas 0.196 1.046

(0.907) (0.977)

lrtwex 0.983* 1.133*

(0.400) (0.507)

befile6 0.0596 -0.0165

(0.261) (0.319)

affile6 -0.0324 -0.0332

(0.264) (0.322)

afdec6 -0.565 -0.577

(0.286) (0.342)

_cons -17.80 -37.08

(21.05) (22.78)

────────────────────────────────────────────

N 131 131

rho 0.293

────────────────────────────────────────────

Standard errors in parentheses

* p<0.05, ** p<0.01, *** p<0.001

There is serial correlation, but we account for it with the PW FGLS estimator

. reg u l.u lchnimp lchempi lgas lrtwex befile6 affile6 afdec6, noconst

Source │ SS df MS Number of obs = 130

─────────────┼────────────────────────────────── F(8, 122) = 640.05

Model │ 43.5543846 8 5.44429807 Prob > F = 0.0000

Residual │ 1.03773198 122 .008506 R-squared = 0.9767

─────────────┼────────────────────────────────── Adj R-squared = 0.9752

Total │ 44.5921166 130 .343016281 Root MSE = .09223

─────────────┬────────────────────────────────────────────────────────────────

u │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

u │

L1. │ .0309497 .0144099 2.15 0.034 .0024239 .0594755

│

lchnimp │ .9801231 .0143516 68.29 0.000 .9517128 1.008534

lchempi │ -2.98055 .0866866 -34.38 0.000 -3.152155 -2.808945

lgas │ .520767 .0203221 25.63 0.000 .4805374 .5609966

lrtwex │ -.7946765 .0568229 -13.99 0.000 -.9071631 -.6821898

befile6 │ -.0135381 .040266 -0.34 0.737 -.0932487 .0661725

affile6 │ .0355207 .0409758 0.87 0.388 -.045595 .1166365

afdec6 │ .5743468 .0450573 12.75 0.000 .4851514 .6635422

─────────────┴────────────────────────────────────────────────────────────────

. drop u

We’ll show another example comparing OLS and Prais-Winsten estimators. We’ll look at the static Phillips curve, which we know has serial correlation.

. use phillips.dta, clear

Set the Time Series

. tsset year

time variable: year, 1948 to 2003

delta: 1 unit

. est clear

OLS

. eststo OLS: reg inf unem if year < 1997

Source │ SS df MS Number of obs = 49

─────────────┼────────────────────────────────── F(1, 47) = 2.62

Model │ 25.6369575 1 25.6369575 Prob > F = 0.1125

Residual │ 460.61979 47 9.80042107 R-squared = 0.0527

─────────────┼────────────────────────────────── Adj R-squared = 0.0326

Total │ 486.256748 48 10.1303489 Root MSE = 3.1306

─────────────┬────────────────────────────────────────────────────────────────

inf │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

unem │ .4676257 .2891262 1.62 0.112 -.1140213 1.049273

_cons │ 1.42361 1.719015 0.83 0.412 -2.034602 4.881822

─────────────┴────────────────────────────────────────────────────────────────

Prais-Winsten

. eststo PW: prais inf unem if year < 1997

Iteration 0: rho = 0.0000

Iteration 1: rho = 0.5727

Iteration 2: rho = 0.7307

Iteration 3: rho = 0.7719

Iteration 4: rho = 0.7792

Iteration 5: rho = 0.7803

Iteration 6: rho = 0.7805

Iteration 7: rho = 0.7805

Iteration 8: rho = 0.7805

Iteration 9: rho = 0.7805

Prais-Winsten AR(1) regression -- iterated estimates

Source │ SS df MS Number of obs = 49

─────────────┼────────────────────────────────── F(1, 47) = 7.39

Model │ 37.9720609 1 37.9720609 Prob > F = 0.0092

Residual │ 241.618458 47 5.14081826 R-squared = 0.1358

─────────────┼────────────────────────────────── Adj R-squared = 0.1174

Total │ 279.590519 48 5.82480248 Root MSE = 2.2673

─────────────┬────────────────────────────────────────────────────────────────

inf │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

unem │ -.715659 .3134522 -2.28 0.027 -1.346244 -.0850744

_cons │ 8.295912 2.23143 3.72 0.001 3.806854 12.78497

─────────────┼────────────────────────────────────────────────────────────────

rho │ .7805446

─────────────┴────────────────────────────────────────────────────────────────

Durbin-Watson statistic (original) 0.802700

Durbin-Watson statistic (transformed) 1.909865

Prais-Winsten with Cochrane-Orcutt Transformation

. eststo PW_CO: prais inf unem if year < 1997, corc

Iteration 0: rho = 0.0000

Iteration 1: rho = 0.5727

Iteration 2: rho = 0.7160

Iteration 3: rho = 0.7611

Iteration 4: rho = 0.7715

Iteration 5: rho = 0.7735

Iteration 6: rho = 0.7740

Iteration 7: rho = 0.7740

Iteration 8: rho = 0.7740

Iteration 9: rho = 0.7741

Iteration 10: rho = 0.7741

Cochrane-Orcutt AR(1) regression -- iterated estimates

Source │ SS df MS Number of obs = 48

─────────────┼────────────────────────────────── F(1, 46) = 4.33

Model │ 22.4790685 1 22.4790685 Prob > F = 0.0430

Residual │ 238.604008 46 5.18704365 R-squared = 0.0861

─────────────┼────────────────────────────────── Adj R-squared = 0.0662

Total │ 261.083076 47 5.55495907 Root MSE = 2.2775

─────────────┬────────────────────────────────────────────────────────────────

inf │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

unem │ -.6653356 .3196035 -2.08 0.043 -1.308664 -.0220071

_cons │ 7.583458 2.38053 3.19 0.003 2.7917 12.37522

─────────────┼────────────────────────────────────────────────────────────────

rho │ .7740512

─────────────┴────────────────────────────────────────────────────────────────

Durbin-Watson statistic (original) 0.802700

Durbin-Watson statistic (transformed) 1.593634

FD

. eststo FD: reg d.inf d.unem if year < 1997

Source │ SS df MS Number of obs = 48

─────────────┼────────────────────────────────── F(1, 46) = 7.18

Model │ 41.8222052 1 41.8222052 Prob > F = 0.0102

Residual │ 267.865933 46 5.82317245 R-squared = 0.1350

─────────────┼────────────────────────────────── Adj R-squared = 0.1162

Total │ 309.688138 47 6.58910932 Root MSE = 2.4131

─────────────┬────────────────────────────────────────────────────────────────

D.inf │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

unem │

D1. │ -.8421708 .3142509 -2.68 0.010 -1.474725 -.2096165

│

_cons │ -.0781776 .3484621 -0.22 0.823 -.7795954 .6232401

─────────────┴────────────────────────────────────────────────────────────────

. esttab, mtitle se stat(N rho)

────────────────────────────────────────────────────────────────────────────

(1) (2) (3) (4)

OLS PW PW_CO FD

────────────────────────────────────────────────────────────────────────────

unem 0.468 -0.716* -0.665*

(0.289) (0.313) (0.320)

D.unem -0.842*

(0.314)

_cons 1.424 8.296*** 7.583** -0.0782

(1.719) (2.231) (2.381) (0.348)

────────────────────────────────────────────────────────────────────────────

N 49 49 48 48

rho 0.781 0.774

────────────────────────────────────────────────────────────────────────────

Standard errors in parentheses

* p<0.05, ** p<0.01, *** p<0.001

The OLS and PW estimators might give very different estimators if our assumptions of strict exogeneity and the a \[ Cov(x_(t+1)+x_(t-1),u_t)=0 \] fail. If that is the case then using OLS with a first-difference might be a better method. We can see that the difference is quite notable. With our OLS estimators, the tradeoff between inflation and employment is non-existent, but with the PW estimator our estimate of beta 1 is closer to our first-difference estimate of beta 1.

It is possible that there is no relationship with the static model, but the change in inflation and the change in unemployment are negatively related.

. use intdef.dta, clear

Set the Time Series

. tsset year

time variable: year, 1948 to 2003

delta: 1 unit

We’ll look at the relationship between interest rates from the 3-month T-bill rate (i3) and inflation rate (inf) and deficits as a percentage of GDP. Static Model

. reg i3 inf def if year < 2004

Source │ SS df MS Number of obs = 56

─────────────┼────────────────────────────────── F(2, 53) = 40.09

Model │ 272.420338 2 136.210169 Prob > F = 0.0000

Residual │ 180.054275 53 3.39725047 R-squared = 0.6021

─────────────┼────────────────────────────────── Adj R-squared = 0.5871

Total │ 452.474612 55 8.22681113 Root MSE = 1.8432

─────────────┬────────────────────────────────────────────────────────────────

i3 │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

inf │ .6058659 .0821348 7.38 0.000 .4411243 .7706074

def │ .5130579 .1183841 4.33 0.000 .2756095 .7505062

_cons │ 1.733266 .431967 4.01 0.000 .8668497 2.599682

─────────────┴────────────────────────────────────────────────────────────────

Get Durban-Watson Statistic

. dwstat Durbin-Watson d-statistic( 3, 56) = .7161527

Critical values d(3,56)=.716, at the 5% level dL = 1.452 dU=1.681 dwstat < dL so we reject the null hypothesis

. predict u, resid

. reg u l.u, noconst

Source │ SS df MS Number of obs = 55

─────────────┼────────────────────────────────── F(1, 54) = 32.83

Model │ 64.1034163 1 64.1034163 Prob > F = 0.0000

Residual │ 105.448636 54 1.95275252 R-squared = 0.3781

─────────────┼────────────────────────────────── Adj R-squared = 0.3666

Total │ 169.552053 55 3.08276459 Root MSE = 1.3974

─────────────┬────────────────────────────────────────────────────────────────

u │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

u │

L1. │ .6228816 .1087148 5.73 0.000 .4049216 .8408415

─────────────┴────────────────────────────────────────────────────────────────

. drop u

We find that we have notable serial correlation in the error term that is statistically significant. We’ll run a first-difference model next.

First differencing

. reg d.i3 d.inf d.def if year < 2004

Source │ SS df MS Number of obs = 55

─────────────┼────────────────────────────────── F(2, 52) = 5.57

Model │ 17.8058164 2 8.90290822 Prob > F = 0.0065

Residual │ 83.1753707 52 1.59952636 R-squared = 0.1763

─────────────┼────────────────────────────────── Adj R-squared = 0.1446

Total │ 100.981187 54 1.87002198 Root MSE = 1.2647

─────────────┬────────────────────────────────────────────────────────────────

D.i3 │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

inf │

D1. │ .1494892 .0921555 1.62 0.111 -.0354343 .3344127

│

def │

D1. │ -.1813151 .1476825 -1.23 0.225 -.4776618 .1150315

│

_cons │ .0417738 .1713874 0.24 0.808 -.3021401 .3856877

─────────────┴────────────────────────────────────────────────────────────────

. dwstat

Durbin-Watson d-statistic( 3, 55) = 1.796365

Critical values d(3,56)=1.796, at the 5% level dL = 1.452 dU=1.681 dwstat > dU so we fail to reject the null hypothesis

. predict u, resid

(1 missing value generated)

. reg u l.u, noconst

Source │ SS df MS Number of obs = 54

─────────────┼────────────────────────────────── F(1, 53) = 0.29

Model │ .427058269 1 .427058269 Prob > F = 0.5921

Residual │ 77.8807184 53 1.46944752 R-squared = 0.0055

─────────────┼────────────────────────────────── Adj R-squared = -0.0133

Total │ 78.3077766 54 1.45014401 Root MSE = 1.2122

─────────────┬────────────────────────────────────────────────────────────────

u │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

u │

L1. │ .0717246 .133046 0.54 0.592 -.1951318 .3385811

─────────────┴────────────────────────────────────────────────────────────────

The serial correlation is no longer a problem with our first difference model, since first differencing can transform a unit root process I(1) into a I(0) process.

with Heteroskedastic and Autocorrelation Consistent (HAC) standard errors.

. use prminwge.dta, clear

We’ll revisit our Puerto Rican examination of the impact of minimum wage importance We’ll use Heteroskedastic and Autocorrelation Consistent (HAC) standard errors, and we’ll compare OLS, OLS with HAC standard errors, and Prais-Winsten estimates We’ll allow a maximum lag order of autocorrelation up to 2 with the lag(2) option.

Set Time Series

. tsset year, yearly

time variable: year, 1950 to 1987

delta: 1 year

. est clear

OLS

. eststo OLS: reg lprepop lmincov lprgnp lusgnp t if year < 1988

Source │ SS df MS Number of obs = 38

─────────────┼────────────────────────────────── F(4, 33) = 66.23

Model │ .284430187 4 .071107547 Prob > F = 0.0000

Residual │ .035428331 33 .001073586 R-squared = 0.8892

─────────────┼────────────────────────────────── Adj R-squared = 0.8758

Total │ .319858518 37 .008644825 Root MSE = .03277

─────────────┬────────────────────────────────────────────────────────────────

lprepop │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lmincov │ -.2122612 .0401524 -5.29 0.000 -.2939518 -.1305706

lprgnp │ .2852386 .0804922 3.54 0.001 .121476 .4490012

lusgnp │ .4860463 .2219829 2.19 0.036 .0344188 .9376739

t │ -.0266633 .0046267 -5.76 0.000 -.0360765 -.0172502

_cons │ -6.663432 1.257831 -5.30 0.000 -9.222508 -4.104356

─────────────┴────────────────────────────────────────────────────────────────

Newey with lag order 1

. eststo Newey1: newey lprepop lmincov lprgnp lusgnp t if year < 1988, lag(1)

Regression with Newey-West standard errors Number of obs = 38

maximum lag: 1 F( 4, 33) = 40.98

Prob > F = 0.0000

─────────────┬────────────────────────────────────────────────────────────────

│ Newey-West

lprepop │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lmincov │ -.2122612 .0454552 -4.67 0.000 -.3047405 -.119782

lprgnp │ .2852386 .1001564 2.85 0.008 .081469 .4890083

lusgnp │ .4860463 .27194 1.79 0.083 -.0672197 1.039312

t │ -.0266633 .0054879 -4.86 0.000 -.0378285 -.0154981

_cons │ -6.663432 1.475245 -4.52 0.000 -9.664841 -3.662023

─────────────┴────────────────────────────────────────────────────────────────

Newey with lag order 2

. eststo Newey2: newey lprepop lmincov lprgnp lusgnp t if year < 1988, lag(2)

Regression with Newey-West standard errors Number of obs = 38

maximum lag: 2 F( 4, 33) = 37.84

Prob > F = 0.0000

─────────────┬────────────────────────────────────────────────────────────────

│ Newey-West

lprepop │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lmincov │ -.2122612 .0457187 -4.64 0.000 -.3052766 -.1192459

lprgnp │ .2852386 .0996361 2.86 0.007 .0825275 .4879497

lusgnp │ .4860463 .2791124 1.74 0.091 -.0818122 1.053905

t │ -.0266633 .0057558 -4.63 0.000 -.0383736 -.014953

_cons │ -6.663432 1.536433 -4.34 0.000 -9.789329 -3.537535

─────────────┴────────────────────────────────────────────────────────────────

Prais-Winsten

. eststo PW: prais lprepop lmincov lprgnp lusgnp t if year < 1988

Iteration 0: rho = 0.0000

Iteration 1: rho = 0.4197

Iteration 2: rho = 0.5325

Iteration 3: rho = 0.5796

Iteration 4: rho = 0.5999

Iteration 5: rho = 0.6086

Iteration 6: rho = 0.6123

Iteration 7: rho = 0.6139

Iteration 8: rho = 0.6146

Iteration 9: rho = 0.6149

Iteration 10: rho = 0.6150

Iteration 11: rho = 0.6151

Iteration 12: rho = 0.6151

Iteration 13: rho = 0.6151

Iteration 14: rho = 0.6151

Iteration 15: rho = 0.6151

Iteration 16: rho = 0.6151

Prais-Winsten AR(1) regression -- iterated estimates

Source │ SS df MS Number of obs = 38

─────────────┼────────────────────────────────── F(4, 33) = 24.87

Model │ .080888012 4 .020222003 Prob > F = 0.0000

Residual │ .026835918 33 .00081321 R-squared = 0.7509

─────────────┼────────────────────────────────── Adj R-squared = 0.7207

Total │ .10772393 37 .002911458 Root MSE = .02852

─────────────┬────────────────────────────────────────────────────────────────

lprepop │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lmincov │ -.1477111 .0458423 -3.22 0.003 -.2409779 -.0544443

lprgnp │ .2513828 .1164623 2.16 0.038 .0144384 .4883271

lusgnp │ .2557114 .2317498 1.10 0.278 -.2157872 .72721

t │ -.0205016 .005856 -3.50 0.001 -.0324158 -.0085875

_cons │ -4.652853 1.37647 -3.38 0.002 -7.453303 -1.852404

─────────────┼────────────────────────────────────────────────────────────────

rho │ .6151374

─────────────┴────────────────────────────────────────────────────────────────

Durbin-Watson statistic (original) 1.013709

Durbin-Watson statistic (transformed) 1.736277

With t-stats below estimated parameters

. esttab, mtitle scalars(F N)

────────────────────────────────────────────────────────────────────────────

(1) (2) (3) (4)

OLS Newey1 Newey2 PW

────────────────────────────────────────────────────────────────────────────

lmincov -0.212*** -0.212*** -0.212*** -0.148**

(-5.29) (-4.67) (-4.64) (-3.22)

lprgnp 0.285** 0.285** 0.285** 0.251*

(3.54) (2.85) (2.86) (2.16)

lusgnp 0.486* 0.486 0.486 0.256

(2.19) (1.79) (1.74) (1.10)

t -0.0267*** -0.0267*** -0.0267*** -0.0205**

(-5.76) (-4.86) (-4.63) (-3.50)

_cons -6.663*** -6.663*** -6.663*** -4.653**

(-5.30) (-4.52) (-4.34) (-3.38)

────────────────────────────────────────────────────────────────────────────

N 38 38 38 38

F 66.23 40.98 37.84 24.87

────────────────────────────────────────────────────────────────────────────

t statistics in parentheses

* p<0.05, ** p<0.01, *** p<0.001

With standard errors below the estimated parameters

. esttab, mtitle se scalars(F N)

────────────────────────────────────────────────────────────────────────────

(1) (2) (3) (4)

OLS Newey1 Newey2 PW

────────────────────────────────────────────────────────────────────────────

lmincov -0.212*** -0.212*** -0.212*** -0.148**

(0.0402) (0.0455) (0.0457) (0.0458)

lprgnp 0.285** 0.285** 0.285** 0.251*

(0.0805) (0.100) (0.0996) (0.116)

lusgnp 0.486* 0.486 0.486 0.256

(0.222) (0.272) (0.279) (0.232)

t -0.0267*** -0.0267*** -0.0267*** -0.0205**

(0.00463) (0.00549) (0.00576) (0.00586)

_cons -6.663*** -6.663*** -6.663*** -4.653**

(1.258) (1.475) (1.536) (1.376)

────────────────────────────────────────────────────────────────────────────

N 38 38 38 38

F 66.23 40.98 37.84 24.87

────────────────────────────────────────────────────────────────────────────

Standard errors in parentheses

* p<0.05, ** p<0.01, *** p<0.001

Notice how our t-stat have fallen and our standard errors have risen for our Newey1 and Newey2 compared to OLS. Also, notice how the Prais-Winsten beta-hat on minimum coverage is closer to 0, then OLS or OLS with HAC standard errors.

. use nyse.dta, clear

We’ll revisit our test of the Efficient Market Hypothesis with stock return data. We can test to see if our assumption of homoskedasticity is valid with our time series. This is a separate test than the test for serial correlation.

Set TIME Series

. tsset t, weekly

time variable: t, 1960w2 to 1973w16

delta: 1 week

OLS

. reg return l.return

Source │ SS df MS Number of obs = 689

─────────────┼────────────────────────────────── F(1, 687) = 2.40

Model │ 10.6866231 1 10.6866231 Prob > F = 0.1218

Residual │ 3059.73817 687 4.45376735 R-squared = 0.0035

─────────────┼────────────────────────────────── Adj R-squared = 0.0020

Total │ 3070.42479 688 4.46282673 Root MSE = 2.1104

─────────────┬────────────────────────────────────────────────────────────────

return │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

return │

L1. │ .0588984 .0380231 1.55 0.122 -.0157569 .1335538

│

_cons │ .179634 .0807419 2.22 0.026 .0211034 .3381646

─────────────┴────────────────────────────────────────────────────────────────

We’ll test heteroskedasticity with estat hettest

. estat hettest

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

Ho: Constant variance

Variables: fitted values of return

chi2(1) = 95.22

Prob > chi2 = 0.0000

We’ll manually calculate the Breusch-Pagan test

. predict u, residu

(2 missing values generated)

. gen u2=u^2

(2 missing values generated)

. reg u2 l.return

Source │ SS df MS Number of obs = 689

─────────────┼────────────────────────────────── F(1, 687) = 30.05

Model │ 3755.56877 1 3755.56877 Prob > F = 0.0000

Residual │ 85846.2961 687 124.958219 R-squared = 0.0419

─────────────┼────────────────────────────────── Adj R-squared = 0.0405

Total │ 89601.8649 688 130.235269 Root MSE = 11.178

─────────────┬────────────────────────────────────────────────────────────────

u2 │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

return │

L1. │ -1.104133 .2014029 -5.48 0.000 -1.499572 -.7086934

│

_cons │ 4.656501 .4276789 10.89 0.000 3.816786 5.496216

─────────────┴────────────────────────────────────────────────────────────────

Test for serial correlation

. reg u l.u, noconst

Source │ SS df MS Number of obs = 688

─────────────┼────────────────────────────────── F(1, 687) = 0.00

Model │ .00603936 1 .00603936 Prob > F = 0.9706

Residual │ 3059.08227 687 4.45281262 R-squared = 0.0000

─────────────┼────────────────────────────────── Adj R-squared = -0.0015

Total │ 3059.08831 688 4.44634929 Root MSE = 2.1102

─────────────┬────────────────────────────────────────────────────────────────

u │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

u │

L1. │ .001405 .0381496 0.04 0.971 -.0734987 .0763087

─────────────┴────────────────────────────────────────────────────────────────

We can see we reject the null hypothesis that the variance of the error term is constant, and heteroskedasticity is a problem.

We can use robust, or HAC standard errors, but since serial correlation is not a problem, then we don’t need newey estimator.

. reg return l.return, robust

Linear regression Number of obs = 689

F(1, 687) = 0.72

Prob > F = 0.3950

R-squared = 0.0035

Root MSE = 2.1104

─────────────┬────────────────────────────────────────────────────────────────

│ Robust

return │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

return │

L1. │ .0588984 .0692053 0.85 0.395 -.0769809 .1947777

│

_cons │ .179634 .0852916 2.11 0.036 .0121705 .3470975

─────────────┴────────────────────────────────────────────────────────────────

. newey return l.return, lag(1)

Regression with Newey-West standard errors Number of obs = 689

maximum lag: 1 F( 1, 687) = 0.74

Prob > F = 0.3895

─────────────┬────────────────────────────────────────────────────────────────

│ Newey-West

return │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

return │

L1. │ .0588984 .0684001 0.86 0.389 -.0754 .1931968

│

_cons │ .179634 .0855634 2.10 0.036 .0116369 .3476311

─────────────┴────────────────────────────────────────────────────────────────

Expected value does not depend on past returns, but the variance of the error term is not constant, and needs to be corrected.

. use phillips.dta, clear

We’ll use our Phillip’s Curve data to forecast unemployment one-step into the future

Set Time Series

. tsset year

time variable: year, 1948 to 2003

delta: 1 unit

tsline

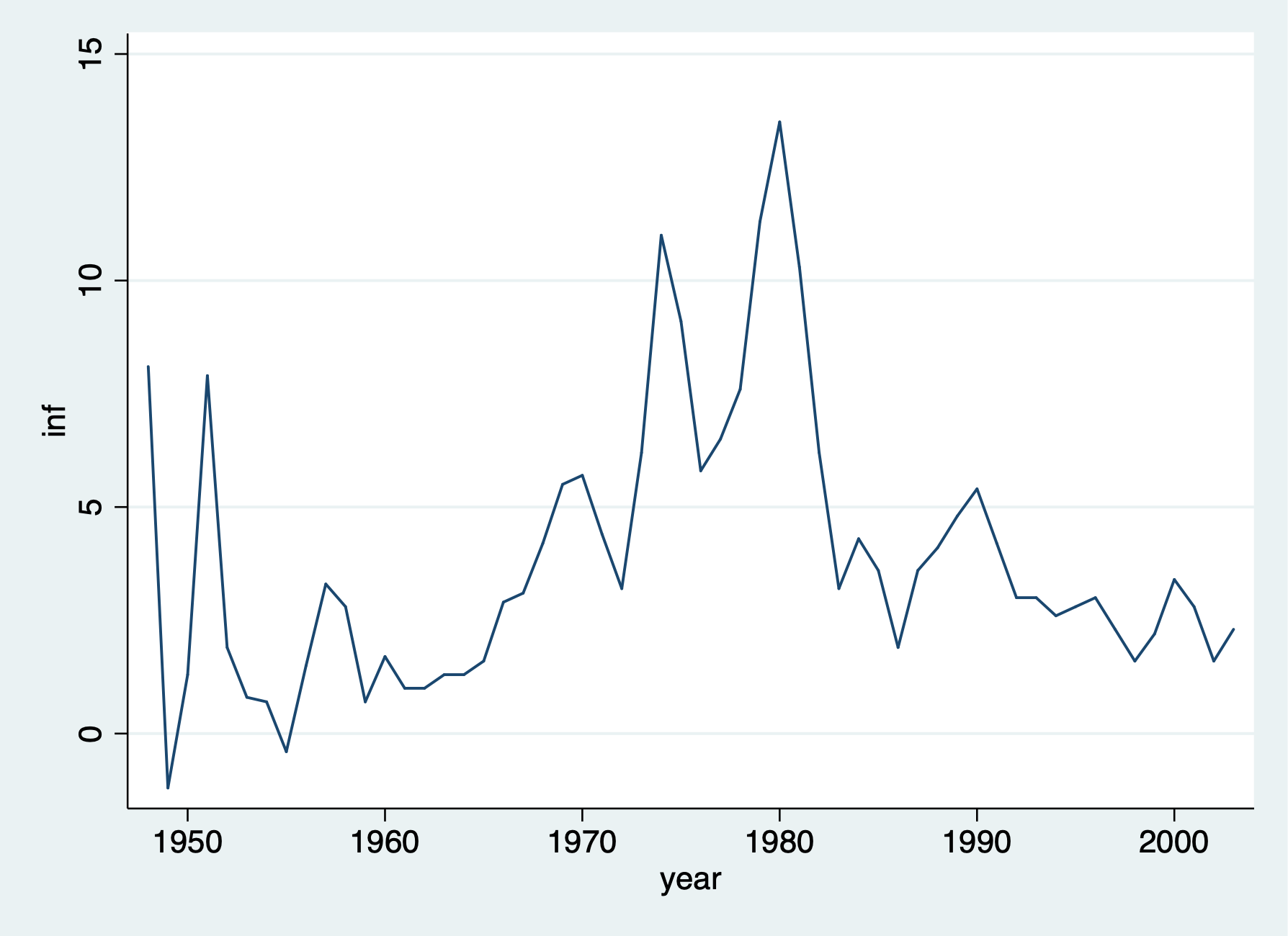

. tsline inf . graph export "/Users/Sam/Desktop/Econ 645/Stata/week_11_inflation.png", replace (file /Users/Sam/Desktop/Econ 645/Stata/week_11_inflation.png written in PNG format)

First we need to Generate training and test samples, so we’ll use the time series sequence until 1996 as our training data, and we’ll use 1997 to 2003 as our testing data.

. gen test = 0 . replace test = 1 if year >= 1997 (7 real changes made) . label define test1 0 "training sample" 1 "testing sample" . label values test test1We’ll use two models to forecast unemployment:

Compare models OLS AR(1)

. reg unem l.unem if test == 0

Source │ SS df MS Number of obs = 48

─────────────┼────────────────────────────────── F(1, 46) = 57.13

Model │ 62.8162728 1 62.8162728 Prob > F = 0.0000

Residual │ 50.5768515 46 1.09949677 R-squared = 0.5540

─────────────┼────────────────────────────────── Adj R-squared = 0.5443

Total │ 113.393124 47 2.41261967 Root MSE = 1.0486

─────────────┬────────────────────────────────────────────────────────────────

unem │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

unem │

L1. │ .7323538 .0968906 7.56 0.000 .537323 .9273845

│

_cons │ 1.571741 .5771181 2.72 0.009 .4100629 2.73342

─────────────┴────────────────────────────────────────────────────────────────

VAR - Add Lagged Inflation

. reg unem l.unem l.inf if test == 0

Source │ SS df MS Number of obs = 48

─────────────┼────────────────────────────────── F(2, 45) = 50.22

Model │ 78.3083336 2 39.1541668 Prob > F = 0.0000

Residual │ 35.0847907 45 .779662015 R-squared = 0.6906

─────────────┼────────────────────────────────── Adj R-squared = 0.6768

Total │ 113.393124 47 2.41261967 Root MSE = .88298

─────────────┬────────────────────────────────────────────────────────────────

unem │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

unem │

L1. │ .6470261 .0838056 7.72 0.000 .4782329 .8158192

│

inf │

L1. │ .1835766 .0411828 4.46 0.000 .1006302 .2665231

│

_cons │ 1.303797 .4896861 2.66 0.011 .3175188 2.290076

─────────────┴────────────────────────────────────────────────────────────────

One-step ahead we can use predict or forecast for AR(1)

. quietly reg unem l.unem if test == 0 . estimates store model1

We can get one-step ahead just using predict

. predict unem_est (option xb assumed; fitted values) (1 missing value generated)

Forecast - One-step-ahead forecast

. forecast create forecast1, replace (Forecast model forecast2 ended.) Forecast model forecast1 started. . forecast estimates model1 Added estimation results from regress. Forecast model forecast1 now contains 1 endogenous variable.

For a one-step ahead forecast, static is our key option otherwise it will not be a one-step ahead forecast.

. forecast solve, prefix(st_) begin(1997) end(2003) static Computing static forecasts for model forecast1. ─────────────────────────────────────────────── Starting period: 1997 Ending period: 2003 Forecast prefix: st_ 1997: ............. 1998: ............. 1999: .............. 2000: .............. 2001: .............. 2002: ............. 2003: ............ Forecast 1 variable spanning 7 periods. ───────────────────────────────────────

Dynamic model - We won’t use l.unem but l.dy_unem

. forecast solve, prefix(dy_) begin(1997) end(2003) Computing dynamic forecasts for model forecast1. ──────────────────────────────────────────────── Starting period: 1997 Ending period: 2003 Forecast prefix: dy_ 1997: ............. 1998: ............. 1999: ............ 2000: ............ 2001: ............ 2002: ............ 2003: ............ Forecast 1 variable spanning 7 periods. ───────────────────────────────────────

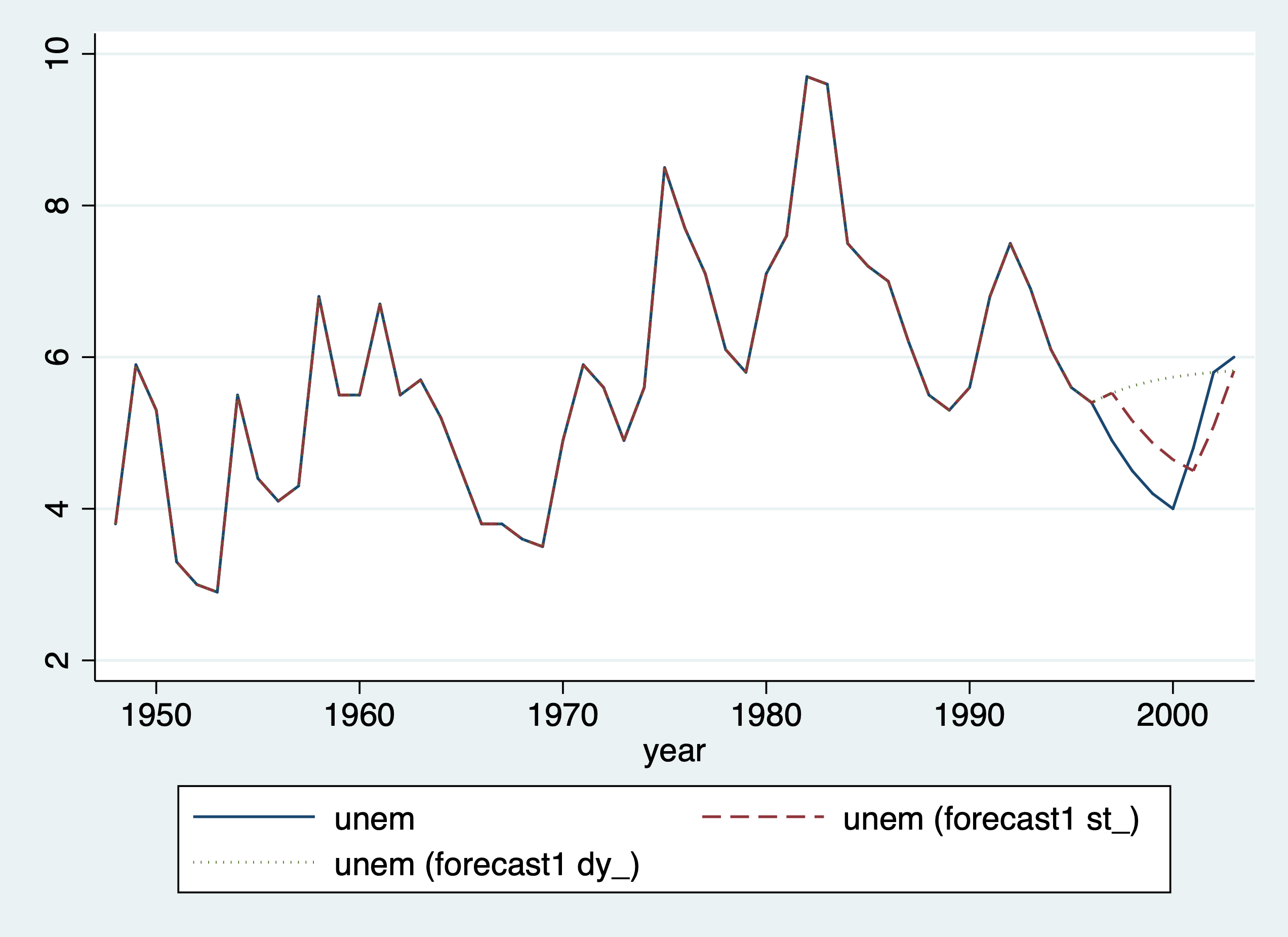

Graph Actual, One-Step-Ahead Model, and Dynamic Model

. twoway line unem year || line st_unem year, lpattern(dash) || line dy_unem year, lpattern(dot) . graph export "/Users/Sam/Desktop/Econ 645/Stata/week_11_static_v_dynamic.png", replace (file /Users/Sam/Desktop/Econ 645/Stata/week_11_static_v_dynamic.png written in PNG format)

Calculate RMSE for Model 1

. gen e = unem - st_unem

. gen e2 = e^2

. sum e2 if test==1

Variable │ Obs Mean Std. Dev. Min Max

─────────────┼─────────────────────────────────────────────────────────

e2 │ 7 .3319141 .1891047 .0326187 .5083123

. scalar esum= `r(sum)'/`r(N)'

. scalar model1_RMSE= esum^.5

. display model1_RMSE

.57611988

Calculate MAE for Model 1

. gen e_abs = abs(e) if test ==1

(49 missing values generated)

. sum e_abs if test==1

Variable │ Obs Mean Std. Dev. Min Max

─────────────┼─────────────────────────────────────────────────────────

e_abs │ 7 .542014 .2109284 .1806064 .7129602

. scalar model1_MAE=`r(mean)'

. display model1_MAE

.54201399

One-step ahead we can use predict or forecast for VAR Model (lagged employment and lagged inflation) Get 1997 estimates

. quietly reg unem l.unem l.inf if year < 1997

Our predict command will produce the same results as forecast solve, static

. predict p2 (option xb assumed; fitted values) (1 missing value generated) . estimates store model2

Forecast for Model 2

. forecast create forecast2, replace (Forecast model forecast1 ended.) Forecast model forecast2 started. . forecast estimates model2 Added estimation results from regress. Forecast model forecast2 now contains 1 endogenous variable.

One-Step-Ahead Forecast of Model 2

. forecast solve, prefix(st2_) begin(1997) end(2003) static Computing static forecasts for model forecast2. ─────────────────────────────────────────────── Starting period: 1997 Ending period: 2003 Forecast prefix: st2_ 1997: ............ 1998: ........... 1999: ........... 2000: ............. 2001: .............. 2002: ............. 2003: .............. Forecast 1 variable spanning 7 periods. ───────────────────────────────────────

Dynamic Forecast of Model 2

. forecast solve, prefix(dy2_) begin(1997) end(2003) Computing dynamic forecasts for model forecast2. ──────────────────────────────────────────────── Starting period: 1997 Ending period: 2003 Forecast prefix: dy2_ 1997: ............ 1998: ............. 1999: ............. 2000: ............ 2001: ............. 2002: ............ 2003: ............. Forecast 1 variable spanning 7 periods. ───────────────────────────────────────

Calculate RMSE for Model 2

. drop e e2 e_abs

. gen e = unem - st2_unem

. gen e2 = e^2

. sum e2 if test==1

Variable │ Obs Mean Std. Dev. Min Max

─────────────┼─────────────────────────────────────────────────────────

e2 │ 7 .2722276 .2459784 .080621 .7681881

. scalar esum2 = `r(sum)'/`r(N)'

. scalar model2_RMSE=esum2^.5

. display model2_RMSE

.52175434

Calculate MAE for Model 2

. gen e_abs = abs(e)

. sum e_abs if test==1

Variable │ Obs Mean Std. Dev. Min Max

─────────────┼─────────────────────────────────────────────────────────

e_abs │ 7 .4841946 .2099534 .2839384 .8764634

. scalar model2_MAE=`r(mean)'

Results

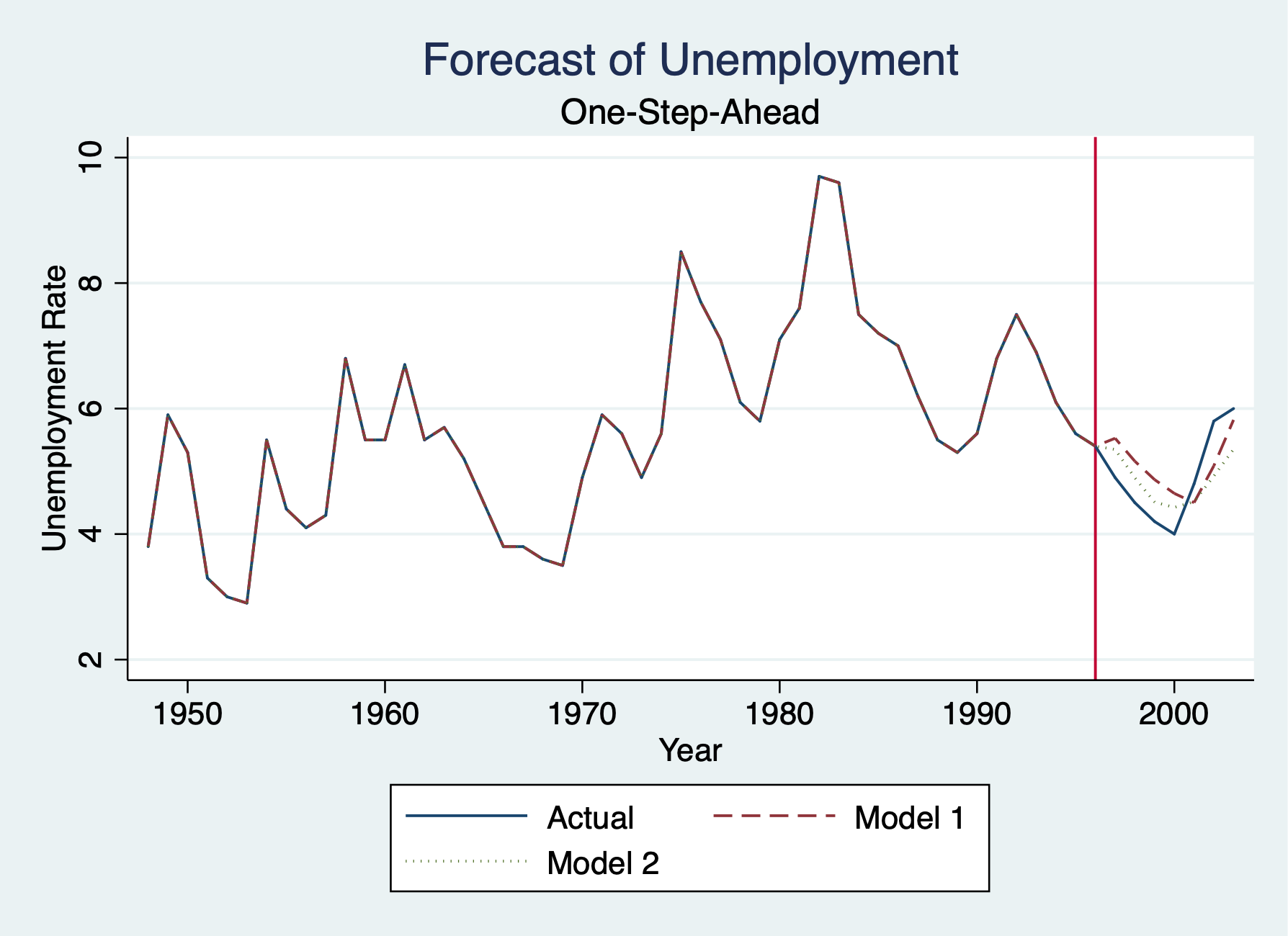

. display "Model 1: RMSE="model1_RMSE " and MAE="model1_MAE Model 1: RMSE=.57611988 and MAE=.54201399 . display "Model 2: RMSE="model2_RMSE " and MAE="model1_MAE Model 2: RMSE=.52175434 and MAE=.54201399 . display "Model 2 with lagged unemployment and lagged inflation has lower RMSE and MAE." Model 2 with lagged unemployment and lagged inflation has lower RMSE and MAE.

Forecasting Line

. twoway line unem year || line st_unem year, lpattern(dash) || line st2_unem year, lpattern(dot) ///

> title("Forecast of Unemployment") xtitle("Year") subtitle("One-Step-Ahead") ytitle("Unemployment Rate") xline(199

> 6) ///

> legend(order(1 "Actual" 2 "Model 1" 3 "Model 2"))

. graph export "/Users/Sam/Desktop/Econ 645/Stata/week_11_forecast.png", replace

(file /Users/Sam/Desktop/Econ 645/Stata/week_11_forecast.png written in PNG format)