Samuel Rowe adapted from Wooldridge

Set Working Directory

. cd "/Users/Sam/Desktop/Econ 645/Data/Wooldridge" /Users/Sam/Desktop/Econ 645/Data/WooldridgeTopics:

. use phillips.dta, clear

*Set the Time Series

. tsset year, yearly

time variable: year, 1948 to 2003

delta: 1 year

. reg inf unem if year < 1997

Source │ SS df MS Number of obs = 49

─────────────┼────────────────────────────────── F(1, 47) = 2.62

Model │ 25.6369575 1 25.6369575 Prob > F = 0.1125

Residual │ 460.61979 47 9.80042107 R-squared = 0.0527

─────────────┼────────────────────────────────── Adj R-squared = 0.0326

Total │ 486.256748 48 10.1303489 Root MSE = 3.1306

─────────────┬────────────────────────────────────────────────────────────────

inf │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

unem │ .4676257 .2891262 1.62 0.112 -.1140213 1.049273

_cons │ 1.42361 1.719015 0.83 0.412 -2.034602 4.881822

─────────────┴────────────────────────────────────────────────────────────────

Our result do not suggest a trade off between inflation and unemployment, and potentially suggest a positive relationship. This is likely a misspecified model and does not best describe the short-run trade-off between inflation and unemployment. We’ll look at an augmented Phillips curve that better describes the relationship.

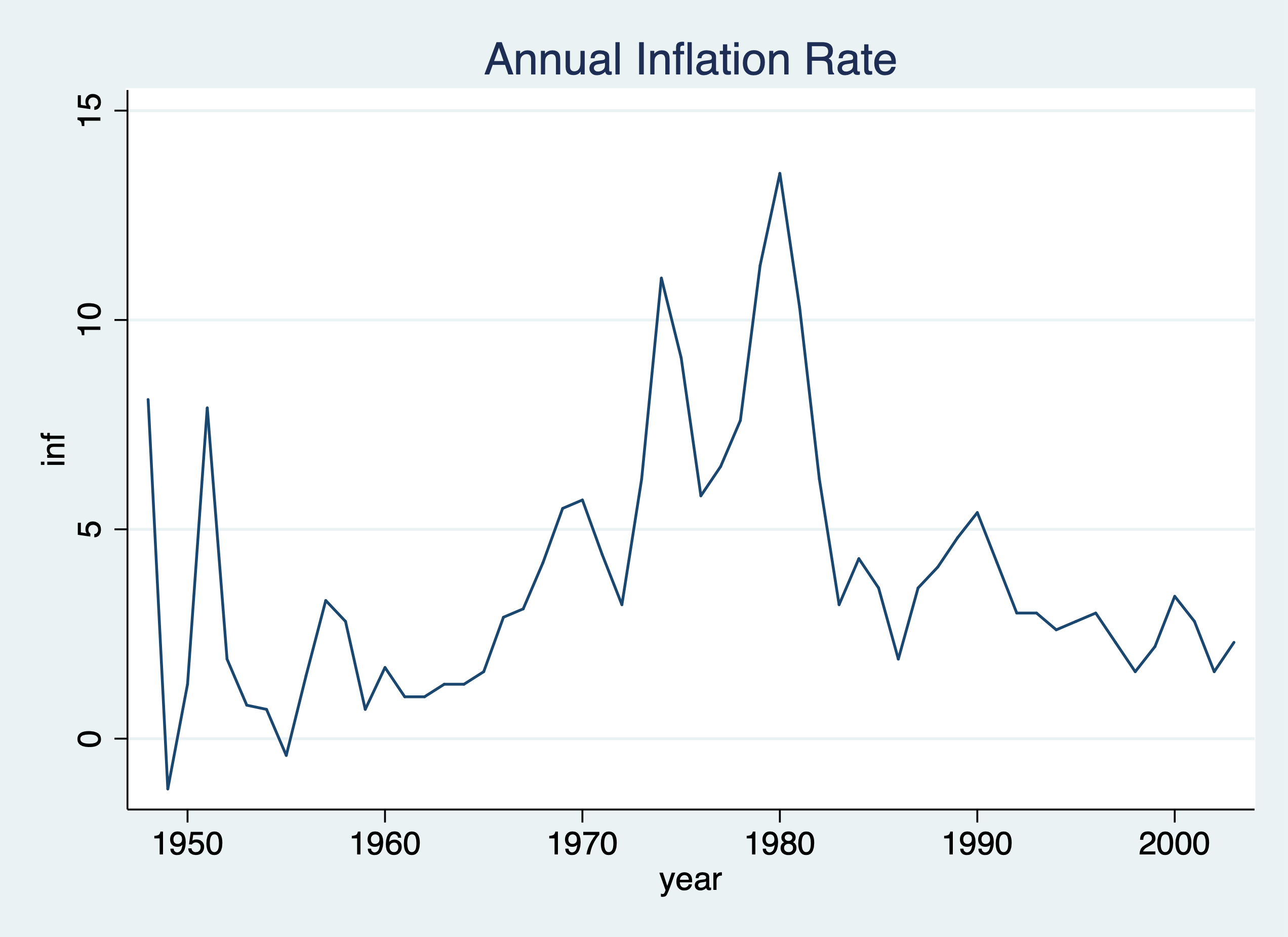

Let’s graph our time series

. twoway line inf year, title("Annual Inflation Rate")

. graph export "/Users/Sam/Desktop/Econ 645/Stata/week_10_inf_line.png", replace

(file /Users/Sam/Desktop/Econ 645/Stata/week_10_inf_line.png written in PNG format)

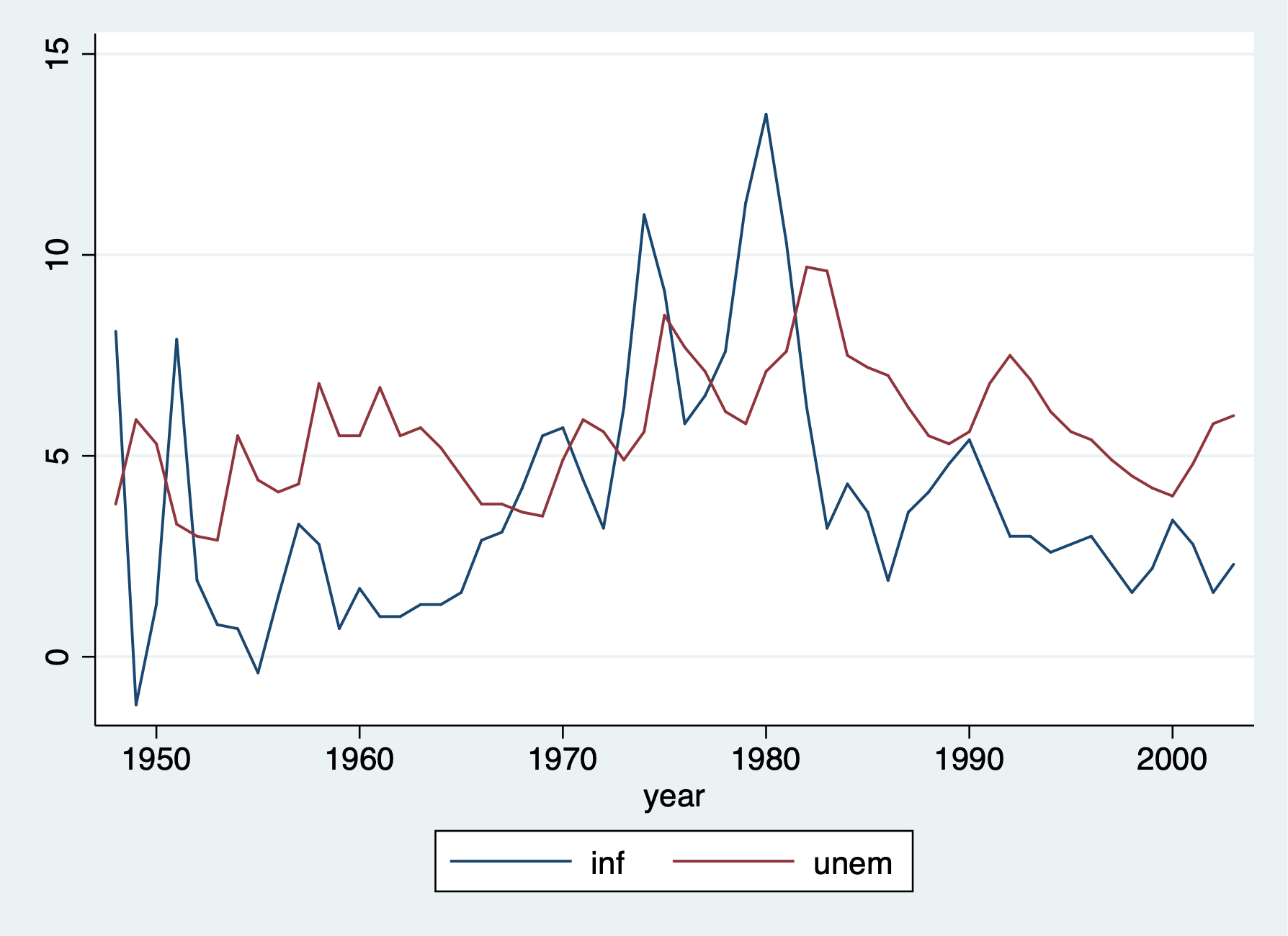

We can use tsline as well.

. tsline inf unem . graph export "/Users/Sam/Desktop/Econ 645/Stata/week_10_ts_infemp.png", replace (file /Users/Sam/Desktop/Econ 645/Stata/week_10_ts_infemp.png written in PNG format)

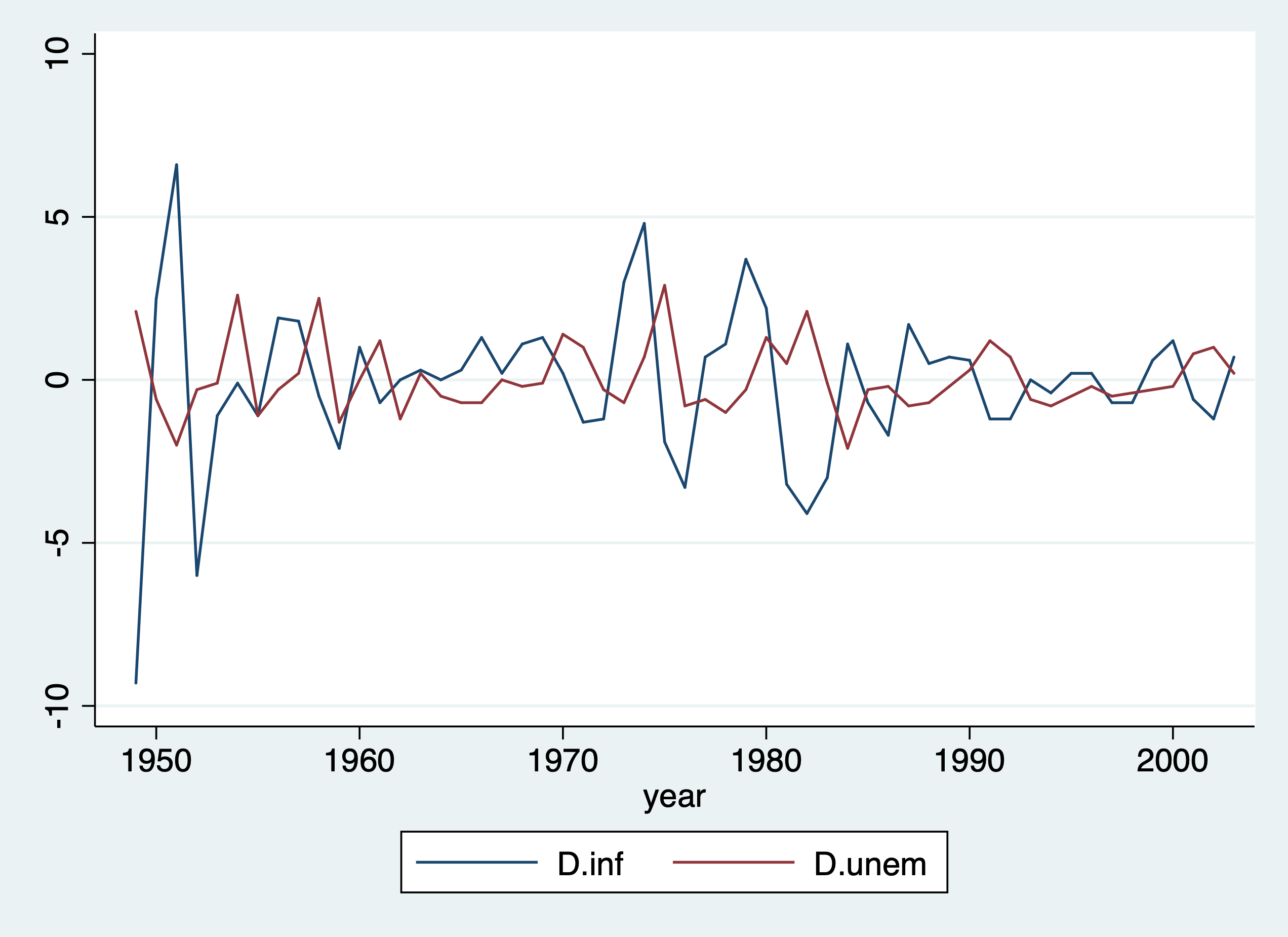

We can take the difference in the time series as well.

. tsline d.inf d.unem . graph export "/Users/Sam/Desktop/Econ 645/Stata/week_10_ts_Dinfemp.png", replace (file /Users/Sam/Desktop/Econ 645/Stata/week_10_ts_Dinfemp.png written in PNG format)

Caution: \[ D2. \neq S2. \] It is not recommended to use d. beyond the first difference. Use the S12. operator If you are interested in \[ x_{t}-x_{t-12} = \Delta x \] D2 gives the difference in differences (not the research design. Such that D2.

operator calculates: \[ D2 = x_{t} - x_{t-1} - (x_{t-1}-x_{t-2}) \] \[ S2 = x_{t} - x_{t-2} \]

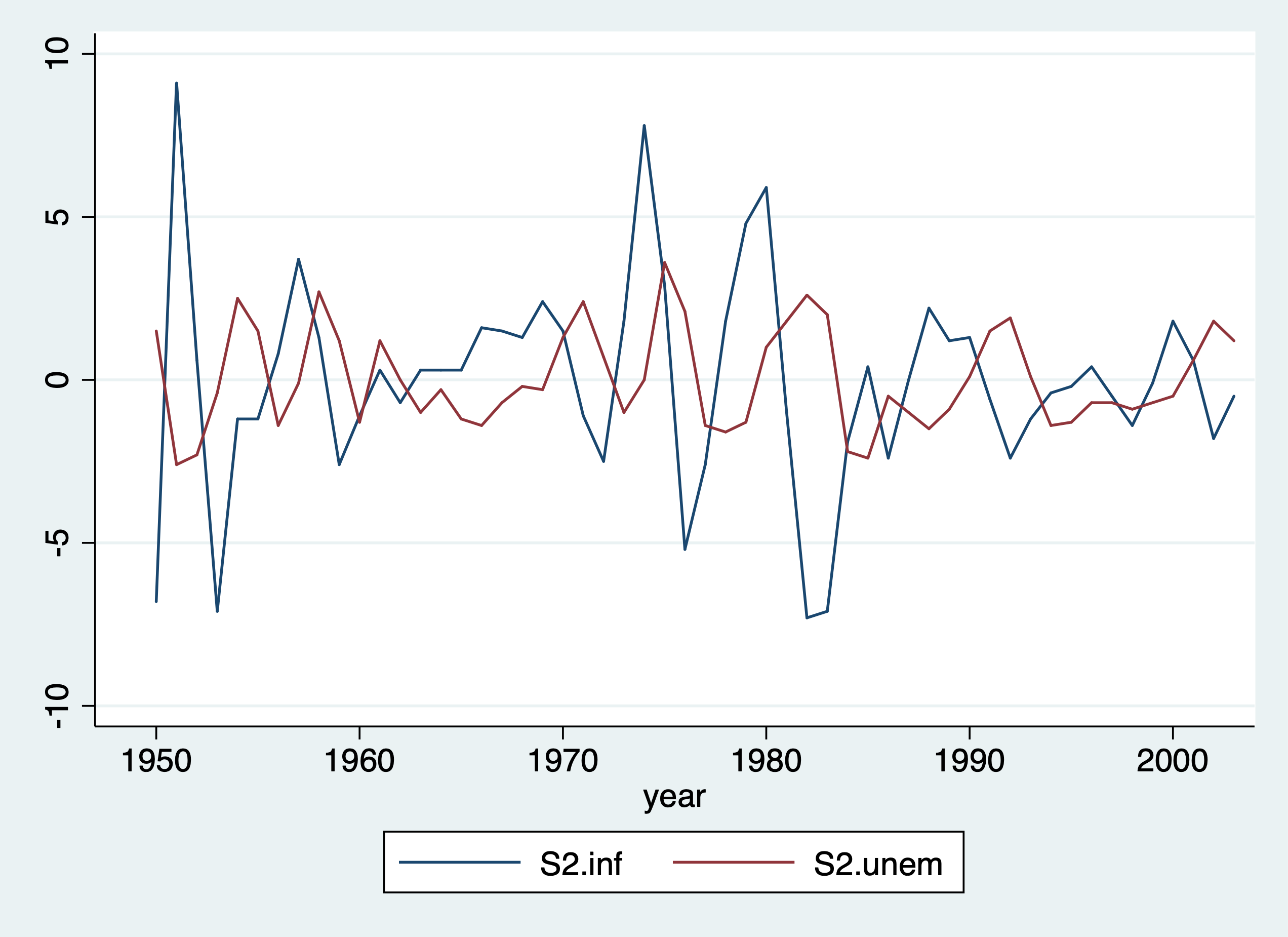

We can take the 12-month difference in the time series as well.

. tsline s2.inf s2.unem . graph export "/Users/Sam/Desktop/Econ 645/Stata/week_10_ts_D12infemp.png", replace (file /Users/Sam/Desktop/Econ 645/Stata/week_10_ts_D12infemp.png written in PNG format)

. use intdef.dta, clearLooking inflation and deficits on interest rates, our model is: \[ i3_t = \beta_0 + \beta_1 inflation_t + \beta_2 deficitpct_t + u_t \] Where

Set the Time Series

. tsset year

time variable: year, 1948 to 2003

delta: 1 unit

. reg i3 inf def if year < 2004

Source │ SS df MS Number of obs = 56

─────────────┼────────────────────────────────── F(2, 53) = 40.09

Model │ 272.420338 2 136.210169 Prob > F = 0.0000

Residual │ 180.054275 53 3.39725047 R-squared = 0.6021

─────────────┼────────────────────────────────── Adj R-squared = 0.5871

Total │ 452.474612 55 8.22681113 Root MSE = 1.8432

─────────────┬────────────────────────────────────────────────────────────────

i3 │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

inf │ .6058659 .0821348 7.38 0.000 .4411243 .7706074

def │ .5130579 .1183841 4.33 0.000 .2756095 .7505062

_cons │ 1.733266 .431967 4.01 0.000 .8668497 2.599682

─────────────┴────────────────────────────────────────────────────────────────

This static model better explain interest rates based on basic macroeconomics. Both contemporaneous variables explain current interest rates. A 1 percentage point increase in the inflation rate leads to a 0.6 percentage point increase in the nominal interest rate. A 1 percentage point increase in the deficits as a percentage of GDP leads to a 0.5 percentage point increase in nominal interest rates.

. use prminwge, clearWe’ll look at the association between employment and minimum wage in Puerto Rico. Our model will be: \[ lprepop_t = \beta_0 + \beta_1 lmincov_t + \beta_2 lusgnp + u_t \] Where

Set Time Series

. tsset year

time variable: year, 1950 to 1987

delta: 1 unit

. reg lprepop lmincov lusgnp if year < 1988

Source │ SS df MS Number of obs = 38

─────────────┼────────────────────────────────── F(2, 35) = 34.04

Model │ .211258366 2 .105629183 Prob > F = 0.0000

Residual │ .108600151 35 .003102861 R-squared = 0.6605

─────────────┼────────────────────────────────── Adj R-squared = 0.6411

Total │ .319858518 37 .008644825 Root MSE = .0557

─────────────┬────────────────────────────────────────────────────────────────

lprepop │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lmincov │ -.1544442 .0649015 -2.38 0.023 -.2862011 -.0226872

lusgnp │ -.0121888 .0885134 -0.14 0.891 -.1918806 .167503

_cons │ -1.054423 .7654065 -1.38 0.177 -2.60828 .4994351

─────────────┴────────────────────────────────────────────────────────────────

Our results show that there is a tradeoff between the employment ratio and the importance of minimum wage. A one percent increase in importance of minimum wage the employment-population ratio declines .154 percent.

The barium industry in the U.S. complained to the International Trade Commission that China was dumping (or selling imports at lower prices to undercut domestic producers). First, are imports unusually high before the complaint? Second, do imports change after the dumping complaint?

. use barium.dta, clear

Set Time Series Monthly

. tsset t, monthly

time variable: t, 1960m2 to 1970m12

delta: 1 month

Our model is the \[ lchnimp_t = \beta_0 + \beta_1 lchempi_t + \beta_2 lgas_t + \beta_3 lrtwex_t +\beta_4 befile6_t + \beta_5 affile6_t + \beta_6 afdec6 + u_t \]

. reg lchnimp lchempi lgas lrtwex befile6 affile6 afdec6

Source │ SS df MS Number of obs = 131

─────────────┼────────────────────────────────── F(6, 124) = 9.06

Model │ 19.4051607 6 3.23419346 Prob > F = 0.0000

Residual │ 44.2470875 124 .356831351 R-squared = 0.3049

─────────────┼────────────────────────────────── Adj R-squared = 0.2712

Total │ 63.6522483 130 .489632679 Root MSE = .59735

─────────────┬────────────────────────────────────────────────────────────────

lchnimp │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lchempi │ 3.117193 .4792021 6.50 0.000 2.168718 4.065668

lgas │ .1963504 .9066172 0.22 0.829 -1.598099 1.9908

lrtwex │ .9830183 .4001537 2.46 0.015 .1910022 1.775034

befile6 │ .0595739 .2609699 0.23 0.820 -.4569585 .5761064

affile6 │ -.0324064 .2642973 -0.12 0.903 -.5555249 .490712

afdec6 │ -.565245 .2858352 -1.98 0.050 -1.130993 .0005028

_cons │ -17.803 21.04537 -0.85 0.399 -59.45769 23.85169

─────────────┴────────────────────────────────────────────────────────────────

We see that imports are not higher 6 months before a complaint, and imports are not lower 6 months after a complaint. However, imports are lower 6 months after a positive decision in a complaint by the ITC. The impact is fairly large and imports of barium chloride fall about 43.2% after a positive decision.

Also notice that rtwex is positive, and we would expect that a stronger dollar increase demand for imports, which is about uni-elastic.

. display (exp(-.565)-1)*100 -43.163985

Lesson: using lags in the explanatory variables Personal Exemption on Fertility Rates

. use fertil3.dta, clear

Our interest the general fertility rate, which is the number of children born to every 1,000 women of childbearing age. PE is the average real dollar value of the personal tax exemption and two binary variables for World War II and the introduction of the birth control pill in 1963.

Our contemporenous model is: \[ gfr_t=\beta_0 + \beta_1 pe_t + \beta_2 ww2_t + \beta_3 pill_t + u_t \]

WhereSet Time Series

. tsset year, yearly

time variable: year, 1913 to 1984

delta: 1 year

. reg gfr pe i.ww2 i.pill if year < 1985

Source │ SS df MS Number of obs = 72

─────────────┼────────────────────────────────── F(3, 68) = 20.38

Model │ 13183.6215 3 4394.54049 Prob > F = 0.0000

Residual │ 14664.2739 68 215.651087 R-squared = 0.4734

─────────────┼────────────────────────────────── Adj R-squared = 0.4502

Total │ 27847.8954 71 392.223879 Root MSE = 14.685

─────────────┬────────────────────────────────────────────────────────────────

gfr │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

pe │ .08254 .0296462 2.78 0.007 .0233819 .1416981

1.ww2 │ -24.2384 7.458253 -3.25 0.002 -39.12111 -9.355684

1.pill │ -31.59403 4.081068 -7.74 0.000 -39.73768 -23.45039

_cons │ 98.68176 3.208129 30.76 0.000 92.28003 105.0835

─────────────┴────────────────────────────────────────────────────────────────

World War II reduced the fertility rate by 24.24 births per 1,000 women of child bearing age, while the introduction of the birth control pill reduced the number of birth by 31.59 births per 1,000 women of childbearing age. The personal tax exemption. A one dollar increase in the average real value of the personal tax exemption increases 0.083 births per 1,000 women of child bearing age or a 12 dollar increase in the average real personal tax exemption increases 1 child per 1,000 women of child bearing ago

Next lets add lags in the average real value of the personal tax exemption. Our Finite Distributed Lag model is: \[ gfr_t=\beta_0 + \beta_1 pe_t + \beta_2 pe_{t-1} + \beta_3 pe_{t-2} + \beta_4 ww2_t + \beta_5 pill_t + u_t \]

. reg gfr pe pe_1 pe_2 i.ww2 i.pill if year < 1985

Source │ SS df MS Number of obs = 70

─────────────┼────────────────────────────────── F(5, 64) = 12.73

Model │ 12959.7886 5 2591.95772 Prob > F = 0.0000

Residual │ 13032.6443 64 203.635067 R-squared = 0.4986

─────────────┼────────────────────────────────── Adj R-squared = 0.4594

Total │ 25992.4329 69 376.701926 Root MSE = 14.27

─────────────┬────────────────────────────────────────────────────────────────

gfr │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

pe │ .0726718 .1255331 0.58 0.565 -.1781094 .323453

pe_1 │ -.0057796 .1556629 -0.04 0.970 -.316752 .3051929

pe_2 │ .0338268 .1262574 0.27 0.790 -.2184013 .286055

1.ww2 │ -22.1265 10.73197 -2.06 0.043 -43.56608 -.6869196

1.pill │ -31.30499 3.981559 -7.86 0.000 -39.25907 -23.35091

_cons │ 95.8705 3.281957 29.21 0.000 89.31403 102.427

─────────────┴────────────────────────────────────────────────────────────────

Our personal exemption variables are no longer statistically significiant, but let’s test the joint significance. We might have multicollinearity that bias our standard errors for our PE variables.

. test pe pe_1 pe_2

( 1) pe = 0

( 2) pe_1 = 0

( 3) pe_2 = 0

F( 3, 64) = 3.97

Prob > F = 0.0117

. test pe_1 pe_2

( 1) pe_1 = 0

( 2) pe_2 = 0

F( 2, 64) = 0.05

Prob > F = 0.9480

Our PE variables are jointly significant, but our lags are jointly insignificiant so we’ll use our static model.

For the estimated LRP: .073-.0058+0.034~.101, but we lack a standard error. We’ll need to estimate the standard error. Let \[ \theta_0=\delta_0+\delta_1+\delta_2 \] denote the LRP and write \[ \delta_0 \] in terms of \[ \theta_0 \, , \delta_1 \, and \, \delta_2 \, where \, \delta_0 = \theta_0 - \delta_1 - \delta_2 \] Next substitute for \[ \delta_0 \] \[ gfr_t = \alpha_0 + \delta_0 pe_t + \delta_1 pe_{t-1} + \delta_2 pe_{t-2} + ... \] to get \[ gfr_t = \alpha_0 + (\theta_0 - \delta_1 - \delta_2)pe_t + \delta_1 pe_{t-1} + \delta_2 pe_{t-2} + ... \] \[ gfr_t = \alpha_0 + \theta_0 pe_t + \delta_1 (pe_{t-1} - pe_t) + \delta_2 (pe_{t-2} - pe_t) + \]

We can estimate \[ \hat{\theta}_{0} \] and its standard error. We can regress gfr_t onto pe_t, (pe_(t-1) - pe_t), and (pe_t-2 - pe_t), ww2, and pill

. gen pe_1_1 = pe_1 - pe (1 missing value generated) . gen pe_2_1 = pe_2 - pe (2 missing values generated)

. reg gfr pe pe_1_1 pe_2_1 i.ww2 i.pill

Source │ SS df MS Number of obs = 70

─────────────┼────────────────────────────────── F(5, 64) = 12.73

Model │ 12959.7886 5 2591.95772 Prob > F = 0.0000

Residual │ 13032.6443 64 203.635067 R-squared = 0.4986

─────────────┼────────────────────────────────── Adj R-squared = 0.4594

Total │ 25992.4329 69 376.701926 Root MSE = 14.27

─────────────┬────────────────────────────────────────────────────────────────

gfr │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

pe │ .1007191 .0298027 3.38 0.001 .0411814 .1602568

pe_1_1 │ -.0057796 .1556629 -0.04 0.970 -.316752 .3051929

pe_2_1 │ .0338268 .1262574 0.27 0.790 -.2184013 .286055

1.ww2 │ -22.1265 10.73197 -2.06 0.043 -43.56608 -.6869196

1.pill │ -31.30499 3.981559 -7.86 0.000 -39.25907 -23.35091

_cons │ 95.8705 3.281957 29.21 0.000 89.31403 102.427

─────────────┴────────────────────────────────────────────────────────────────

Our theta-hat is about .101 and significant, so our LRP has an effect on general fertility rates.

. use hseinv.dta, clear

We look at annual housing investement and a housing price index from 1947 to 1988.

Set Time Series

. tsset year, yearly

time variable: year, 1947 to 1988

delta: 1 year

Our model is the natural log of invpc or real per capita housing investment ($1,000) and price be the housing price index where 1982 = 1 (or 100). We’ll assume constant elasticity with our log-log model.

\[ linvpc = \beta_0 + \beta_1 lprice_t + u_t \]

. reg linvpc lprice

Source │ SS df MS Number of obs = 42

─────────────┼────────────────────────────────── F(1, 40) = 10.53

Model │ .254364468 1 .254364468 Prob > F = 0.0024

Residual │ .966255566 40 .024156389 R-squared = 0.2084

─────────────┼────────────────────────────────── Adj R-squared = 0.1886

Total │ 1.22062003 41 .02977122 Root MSE = .15542

─────────────┬────────────────────────────────────────────────────────────────

linvpc │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lprice │ 1.240943 .3824192 3.24 0.002 .4680452 2.013841

_cons │ -.5502345 .0430266 -12.79 0.000 -.6371945 -.4632746

─────────────┴────────────────────────────────────────────────────────────────

Our output shows that a 1 percent increase in the pricing index increases the investment per capita by 1.24 percent (or elastic response). Note: both investment and price have upward trends that we need to account for.

\[ invpc = \beta_0 + \beta_1 lprice_t + \beta_2 t + u_t \]

. reg linvpc lprice t

Source │ SS df MS Number of obs = 42

─────────────┼────────────────────────────────── F(2, 39) = 10.08

Model │ .415945108 2 .207972554 Prob > F = 0.0003

Residual │ .804674927 39 .02063269 R-squared = 0.3408

─────────────┼────────────────────────────────── Adj R-squared = 0.3070

Total │ 1.22062003 41 .02977122 Root MSE = .14364

─────────────┬────────────────────────────────────────────────────────────────

linvpc │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lprice │ -.3809612 .6788352 -0.56 0.578 -1.754035 .9921125

t │ .0098287 .0035122 2.80 0.008 .0027246 .0169328

_cons │ -.9130595 .1356133 -6.73 0.000 -1.187363 -.6387557

─────────────┴────────────────────────────────────────────────────────────────

After accounting for the upward linear trend for both investment per capita and the housing price index, an increase in price is coefficient is now negative, but it is not statistically significant. We probably have serial correlation which will bias our standard errors.

. predict u, resid

. reg u l.u, noconst

Source │ SS df MS Number of obs = 41

─────────────┼────────────────────────────────── F(1, 40) = 11.10

Model │ .170666637 1 .170666637 Prob > F = 0.0019

Residual │ .614779847 40 .015369496 R-squared = 0.2173

─────────────┼────────────────────────────────── Adj R-squared = 0.1977

Total │ .785446484 41 .019157231 Root MSE = .12397

─────────────┬────────────────────────────────────────────────────────────────

u │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

u │

L1. │ .4632581 .1390204 3.33 0.002 .1822874 .7442288

─────────────┴────────────────────────────────────────────────────────────────

. drop u

. use fertil3.dta, clear

We’ll look at fertility again, but we’ll account for a quadratic time trend. First, we’ll estimate a linear time trend, and then we’ll try a quadratic time trend.

Set Time Series

. tsset year, yearly

time variable: year, 1913 to 1984

delta: 1 year

Linear Trend

. reg gfr pe i.ww2 i.pill t if year < 1985

Source │ SS df MS Number of obs = 72

─────────────┼────────────────────────────────── F(4, 67) = 32.84

Model │ 18441.2357 4 4610.30894 Prob > F = 0.0000

Residual │ 9406.65967 67 140.397905 R-squared = 0.6622

─────────────┼────────────────────────────────── Adj R-squared = 0.6420

Total │ 27847.8954 71 392.223879 Root MSE = 11.849

─────────────┬────────────────────────────────────────────────────────────────

gfr │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

pe │ .2788778 .0400199 6.97 0.000 .1989978 .3587578

1.ww2 │ -35.59228 6.297377 -5.65 0.000 -48.1619 -23.02266

1.pill │ .9974479 6.26163 0.16 0.874 -11.50082 13.49571

t │ -1.149872 .1879038 -6.12 0.000 -1.524929 -.7748145

_cons │ 111.7694 3.357765 33.29 0.000 105.0673 118.4716

─────────────┴────────────────────────────────────────────────────────────────

Quadratic Trend Fertility is declining but at a decreasing negatively rate (eventually a positive t^2 takes over t)

. reg gfr pe i.ww2 i.pill c.t##c.t if year < 1985

Source │ SS df MS Number of obs = 72

─────────────┼────────────────────────────────── F(5, 66) = 35.09

Model │ 20236.3981 5 4047.27961 Prob > F = 0.0000

Residual │ 7611.49734 66 115.325717 R-squared = 0.7267

─────────────┼────────────────────────────────── Adj R-squared = 0.7060

Total │ 27847.8954 71 392.223879 Root MSE = 10.739

─────────────┬────────────────────────────────────────────────────────────────

gfr │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

pe │ .3478126 .0402599 8.64 0.000 .2674311 .428194

1.ww2 │ -35.88028 5.707921 -6.29 0.000 -47.27651 -24.48404

1.pill │ -10.11972 6.336094 -1.60 0.115 -22.77014 2.530696

t │ -2.531426 .3893863 -6.50 0.000 -3.308861 -1.753991

│

c.t#c.t │ .0196126 .004971 3.95 0.000 .0096876 .0295377

│

_cons │ 124.0919 4.360738 28.46 0.000 115.3854 132.7984

─────────────┴────────────────────────────────────────────────────────────────

The fertility rate exhibits upward and downward trends between 1913 and 1984. Interestingly, pe remains fairly robust after adding time trends. The linear time trend shows that general fertility rates are falling by 1.15 childs per 1,000 women of childbearing age for each additional year. However, the quadratic shows that the trend is negative but decreasing rate and will eventually become positive.

The last linear trend is for employment-population ratio and the importance of minimum wage coverage. We’ll add a time trend along with mincov and usgnp.

. use prminwge, clear

Set the Time Series

. tsset year, yearly

time variable: year, 1950 to 1987

delta: 1 year

Add linear trend

. reg lprepop lmincov lusgnp t

Source │ SS df MS Number of obs = 38

─────────────┼────────────────────────────────── F(3, 34) = 62.78

Model │ .270948453 3 .090316151 Prob > F = 0.0000

Residual │ .048910064 34 .001438531 R-squared = 0.8471

─────────────┼────────────────────────────────── Adj R-squared = 0.8336

Total │ .319858518 37 .008644825 Root MSE = .03793

─────────────┬────────────────────────────────────────────────────────────────

lprepop │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lmincov │ -.1686949 .0442463 -3.81 0.001 -.2586142 -.0787757

lusgnp │ 1.057351 .1766369 5.99 0.000 .6983813 1.41632

t │ -.0323542 .0050227 -6.44 0.000 -.0425616 -.0221468

_cons │ -8.696298 1.295764 -6.71 0.000 -11.32961 -6.062988

─────────────┴────────────────────────────────────────────────────────────────

The employment-population ratio does not have much of a downward or upward trend, but usgnp does. Тhe linear trend of usgnp is about 3% per year, so an estimate of 1.06 in our model mean that when usgnp increases by 1% above its long-term trend, employment-population ratio increases by about 1.06%

We’ll add monthly variables to account for the fact that imports are not seasonlly adjusted.

. use barium.dta, clear

Set Time Series Monthly

. tsset t, monthly

time variable: t, 1960m2 to 1970m12

delta: 1 month

. reg lchnimp lchempi lgas lrtwex befile6 affile6 afdec6 feb mar apr may ///

> jun jul aug sep oct nov dec

Source │ SS df MS Number of obs = 131

─────────────┼────────────────────────────────── F(17, 113) = 3.71

Model │ 22.8083523 17 1.34166778 Prob > F = 0.0000

Residual │ 40.843896 113 .361450407 R-squared = 0.3583

─────────────┼────────────────────────────────── Adj R-squared = 0.2618

Total │ 63.6522483 130 .489632679 Root MSE = .60121

─────────────┬────────────────────────────────────────────────────────────────

lchnimp │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

lchempi │ 3.26506 .4929302 6.62 0.000 2.288476 4.241644

lgas │ -1.278121 1.389008 -0.92 0.359 -4.029997 1.473755

lrtwex │ .6630496 .4713038 1.41 0.162 -.2706882 1.596787

befile6 │ .1397024 .2668075 0.52 0.602 -.3888914 .6682962

affile6 │ .0126317 .2786866 0.05 0.964 -.5394967 .5647601

afdec6 │ -.5213006 .30195 -1.73 0.087 -1.119518 .0769168

feb │ -.4177089 .3044445 -1.37 0.173 -1.020868 .1854505

mar │ .0590528 .2647308 0.22 0.824 -.4654266 .5835322

apr │ -.4514825 .2683865 -1.68 0.095 -.9832046 .0802396

may │ .0333085 .2692425 0.12 0.902 -.5001093 .5667264

jun │ -.2063321 .2692515 -0.77 0.445 -.7397679 .3271038

jul │ .0038354 .2787665 0.01 0.989 -.5484513 .5561222

aug │ -.1570652 .2779928 -0.56 0.573 -.7078191 .3936887

sep │ -.1341606 .2676556 -0.50 0.617 -.6644348 .3961135

oct │ .0516921 .2668512 0.19 0.847 -.4769883 .5803725

nov │ -.24626 .2628272 -0.94 0.351 -.766968 .274448

dec │ .1328368 .2714234 0.49 0.626 -.4049019 .6705755

_cons │ 16.77877 32.42865 0.52 0.606 -47.46824 81.02577

─────────────┴────────────────────────────────────────────────────────────────

We compare all months to January as the base period, but let’s test their joint significance.

. test feb mar apr may jun jul aug sep oct nov dec

( 1) feb = 0

( 2) mar = 0

( 3) apr = 0

( 4) may = 0

( 5) jun = 0

( 6) jul = 0

( 7) aug = 0

( 8) sep = 0

( 9) oct = 0

(10) nov = 0

(11) dec = 0

F( 11, 113) = 0.86

Prob > F = 0.5852

We find that they are jointly insignificant and seasonality does not seem to be an issue with barium chloride imports.

We’ll test the a version of the efficient market hypothesis (EMH) by looking at weekly stock return from 1976 to 1989.

. use nyse, clear

*Set Time Series

. tsset t, weekly

time variable: t, 1960w2 to 1973w16

delta: 1 week

Our dependent variable is the weekly percentage return on the New York Stock Exchange. A strict form of the EMH states that information observable to the market prior to week t should not help to predict the return during week t. \[ E(y_t|y_{t-1},y_{t-2},...)=E(y_t) \]

We will test EMH by specifying an AR(1) model and our hypothesis states that beta for y_(t-1) will be equal to 0. We’ll assume that stock returns are serially uncorrelated, so we can safetly assume that they are weakly dependent.

\[ return_t = \beta_0 + \rho return_{t-1} + e_t \]

. reg return l.return

Source │ SS df MS Number of obs = 689

─────────────┼────────────────────────────────── F(1, 687) = 2.40

Model │ 10.6866231 1 10.6866231 Prob > F = 0.1218

Residual │ 3059.73817 687 4.45376735 R-squared = 0.0035

─────────────┼────────────────────────────────── Adj R-squared = 0.0020

Total │ 3070.42479 688 4.46282673 Root MSE = 2.1104

─────────────┬────────────────────────────────────────────────────────────────

return │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

return │

L1. │ .0588984 .0380231 1.55 0.122 -.0157569 .1335538

│

_cons │ .179634 .0807419 2.22 0.026 .0211034 .3381646

─────────────┴────────────────────────────────────────────────────────────────

Or

. reg return return_1

Source │ SS df MS Number of obs = 689

─────────────┼────────────────────────────────── F(1, 687) = 2.40

Model │ 10.6866231 1 10.6866231 Prob > F = 0.1218

Residual │ 3059.73817 687 4.45376735 R-squared = 0.0035

─────────────┼────────────────────────────────── Adj R-squared = 0.0020

Total │ 3070.42479 688 4.46282673 Root MSE = 2.1104

─────────────┬────────────────────────────────────────────────────────────────

return │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

return_1 │ .0588984 .0380231 1.55 0.122 -.0157569 .1335538

_cons │ .179634 .0807419 2.22 0.026 .0211034 .3381646

─────────────┴────────────────────────────────────────────────────────────────

. predict u, resid

(2 missing values generated)

. reg u l.u, noconst

Source │ SS df MS Number of obs = 688

─────────────┼────────────────────────────────── F(1, 687) = 0.00

Model │ .00603936 1 .00603936 Prob > F = 0.9706

Residual │ 3059.08227 687 4.45281262 R-squared = 0.0000

─────────────┼────────────────────────────────── Adj R-squared = -0.0015

Total │ 3059.08831 688 4.44634929 Root MSE = 2.1102

─────────────┬────────────────────────────────────────────────────────────────

u │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

u │

L1. │ .001405 .0381496 0.04 0.971 -.0734987 .0763087

─────────────┴────────────────────────────────────────────────────────────────

. drop u

We cannot reject the null hypothesis under our model, but we do have some evidence of positive serial correlation.

We’ll revisit the Phillips curve

. use phillips.dta, clear

Set Time Series

. tsset year

time variable: year, 1948 to 2003

delta: 1 unit

A linear version of the expections augmented Phillips curve can be written as \[ inf_t - inf^e_t=\beta_1(unemp_t-\mu_0) + e_t \]

Where mu_0 is the natural rate of unemployment and inf^e is the expected rate of inflation formed in year t-1. The difference between actual unemployment and the natural rate is called cyclical unemployment, while the difference between inflation and expected inflation is called unanticipated inflation Our e_t is called our supply shock. If there is a trade-off between inflation and unemployment our beta-hat_1 will be negative.

An assumption is made about inflationary expectations and unders adaptive expectations, the expected value of current inflation depends on recently observed inflation. The expected inflation will be assumed to be equal to last years inflation \[ inf_t - inf_{t-1}=\beta_0 + \beta_1 unemp_t + e_t \] \[ \Delta inf_t =\beta_0 + \beta_1 unemp_t + e_t \]

Where \[ \Delta inf_t=inf_t - inf_{t-1} \] \[ \beta_0 = -\beta_1 \mu_0 \] Since beta_1 is expected to be negative and beta_0 is expected to be positive.

Therefore, under adaptive expectations, the augmented Phillips curve relates the change in inflation to the level of unemployment and a supply shock e_t. We’ll assume assumptions TSC.1-TSC.5 hold.

First Difference in the dependent variable or adaptive expectations of inflation

. reg cinf unem if year < 1997

Source │ SS df MS Number of obs = 48

─────────────┼────────────────────────────────── F(1, 46) = 5.56

Model │ 33.3830007 1 33.3830007 Prob > F = 0.0227

Residual │ 276.305134 46 6.00663335 R-squared = 0.1078

─────────────┼────────────────────────────────── Adj R-squared = 0.0884

Total │ 309.688135 47 6.58910925 Root MSE = 2.4508

─────────────┬────────────────────────────────────────────────────────────────

cinf │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

unem │ -.5425869 .2301559 -2.36 0.023 -1.005867 -.079307

_cons │ 3.030581 1.37681 2.20 0.033 .2592061 5.801955

─────────────┴────────────────────────────────────────────────────────────────

or

. reg d.inf unem if year < 1997

Source │ SS df MS Number of obs = 48

─────────────┼────────────────────────────────── F(1, 46) = 5.56

Model │ 33.3829996 1 33.3829996 Prob > F = 0.0227

Residual │ 276.305138 46 6.00663344 R-squared = 0.1078

─────────────┼────────────────────────────────── Adj R-squared = 0.0884

Total │ 309.688138 47 6.58910932 Root MSE = 2.4508

─────────────┬────────────────────────────────────────────────────────────────

D.inf │ Coef. Std. Err. t P>|t| [95% Conf. Interval]

─────────────┼────────────────────────────────────────────────────────────────

unem │ -.5425869 .2301559 -2.36 0.023 -1.005867 -.079307

_cons │ 3.030581 1.37681 2.20 0.033 .259206 5.801955

─────────────┴────────────────────────────────────────────────────────────────

The trade-off between unanticipated inflation and cyclical unemployment is seen in beta-hat_1. A 1-point increase in unemployment decreases unanticipated inflation by about .54 points.

We can estimate the natural rate of unemployment by dividing beta-hat_0 by negative of beta-hat-1

\[ \mu_{0} = \hat{\beta}_{0} / - \hat{\beta}_{1} \]

. display 3.03/.5425 5.5852535

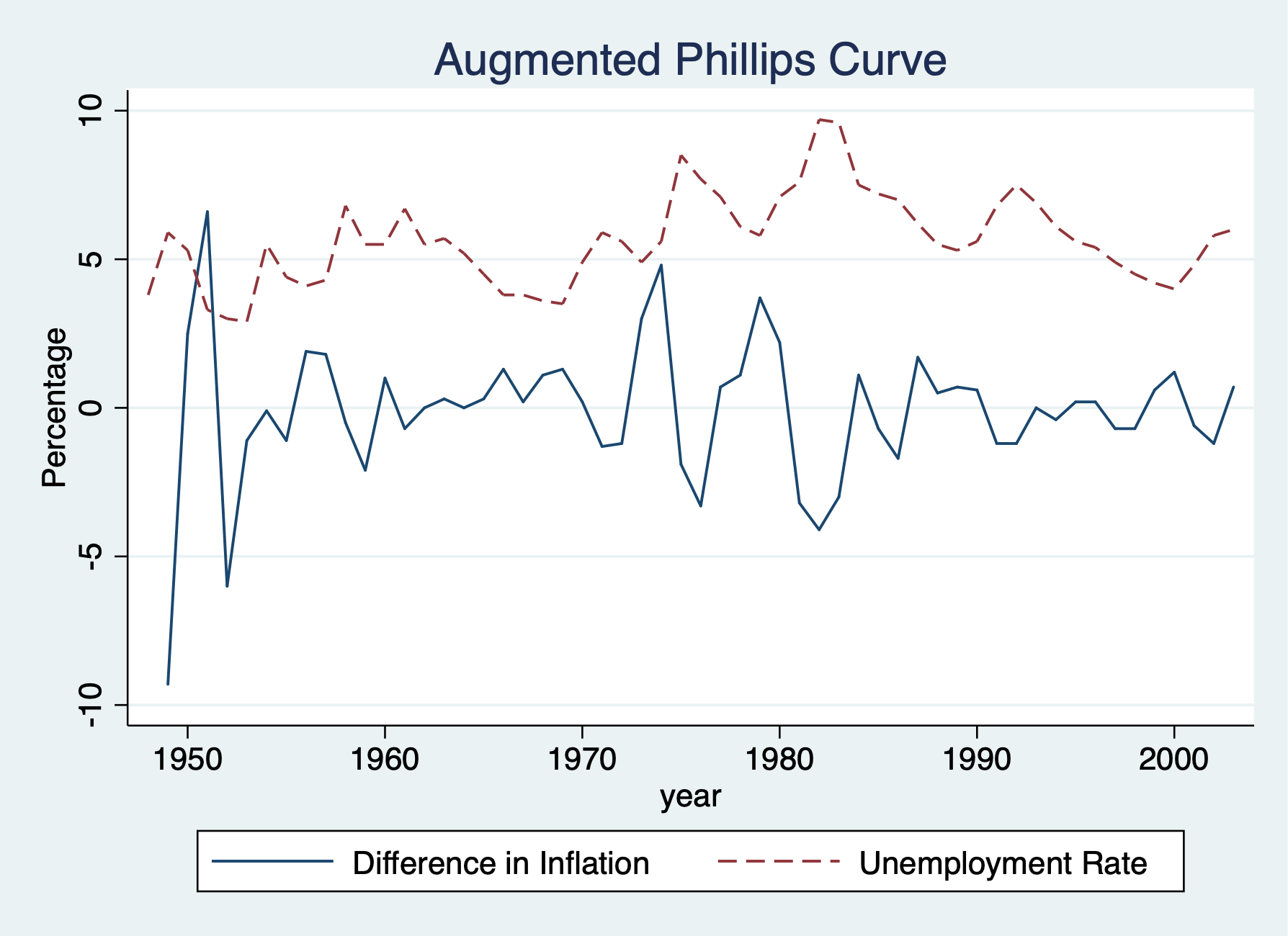

. twoway line cinf year || line unem year, lpattern(dash) ///

> legend(order(1 "Difference in Inflation" 2 "Unemployment Rate")) ///

> title("Augmented Phillips Curve") ytitle(Percentage) xtitle(year)

. graph export "week_10_augmented_phillips.png", replace (file week_10_augmented_phillips.png written in PNG format)